In this paper, we argue that three complementary indicators point to increasing concentration in the S&P 500 market rally:

- A five-year-long outperformance of the (capitalization-weighted) S&P 500 relative to the equally-weighted S&P 500;

- A six-month-long divergence between the (capitalization-weighted) S&P 500 and the ratio of rising-to-falling stocks; and

- A fall in entropy, a better metrics of concentration within the S&P 500, shows that the current degree of concentration, which is largely attributable to Big Tech, is historically high.

This increasing concentration hints at growing imbalances in the economy.

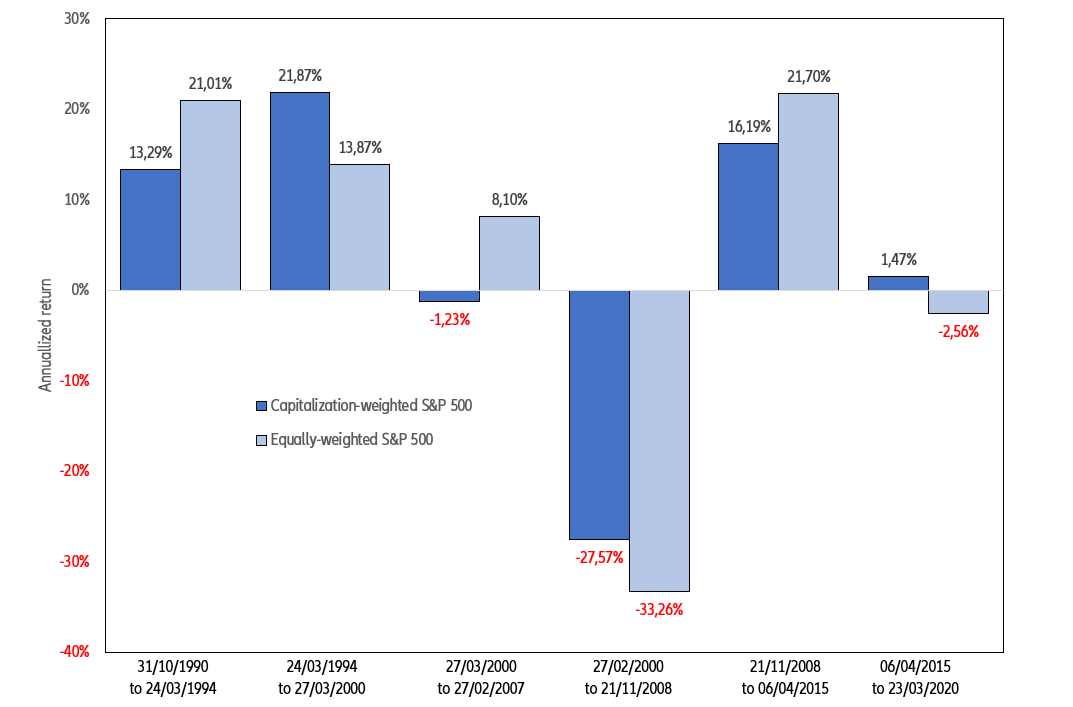

Figure 1 – S&P 500 vs equally-weighted S&P 500 during selected periods

After a period of modest outperformance from April 2015 to March 2020, the capitalization-weighted S&P 500 has been trading sideways relative to its equally-weighted clone ever since 23 March 2020. This over-performance indicates that the largest stocks by market capitalization have outperformed the rest of the market during this period.

Commonly used stock market indices are market capitalization-weighted averages. Such is the case, for example, of the S&P 500 index: the larger the market capitalization of a given constituent stock (number of outstanding shares times share price), the larger its weight. To convince oneself about this, one just needs to compare the annualized rate of return of the S&P 500 with that of its equally weighted clone between selected turning points, as shown in Figure 1. In bull as well as in bear markets,

the capitalization-weighted S&P 500 has sometimes outperformed, sometimes under¬per¬formed the equally weighted S&P 500, most of the time by a large margin. The over-performance of the capitalization-weighted S&P 500 between 24 February and 23 March 2020 confirms the shift to more concentrated gains in a few large-cap stocks (as seen during the dotcom bubble between March 1994 and March 2000 or again between April 2015 and March 2020).

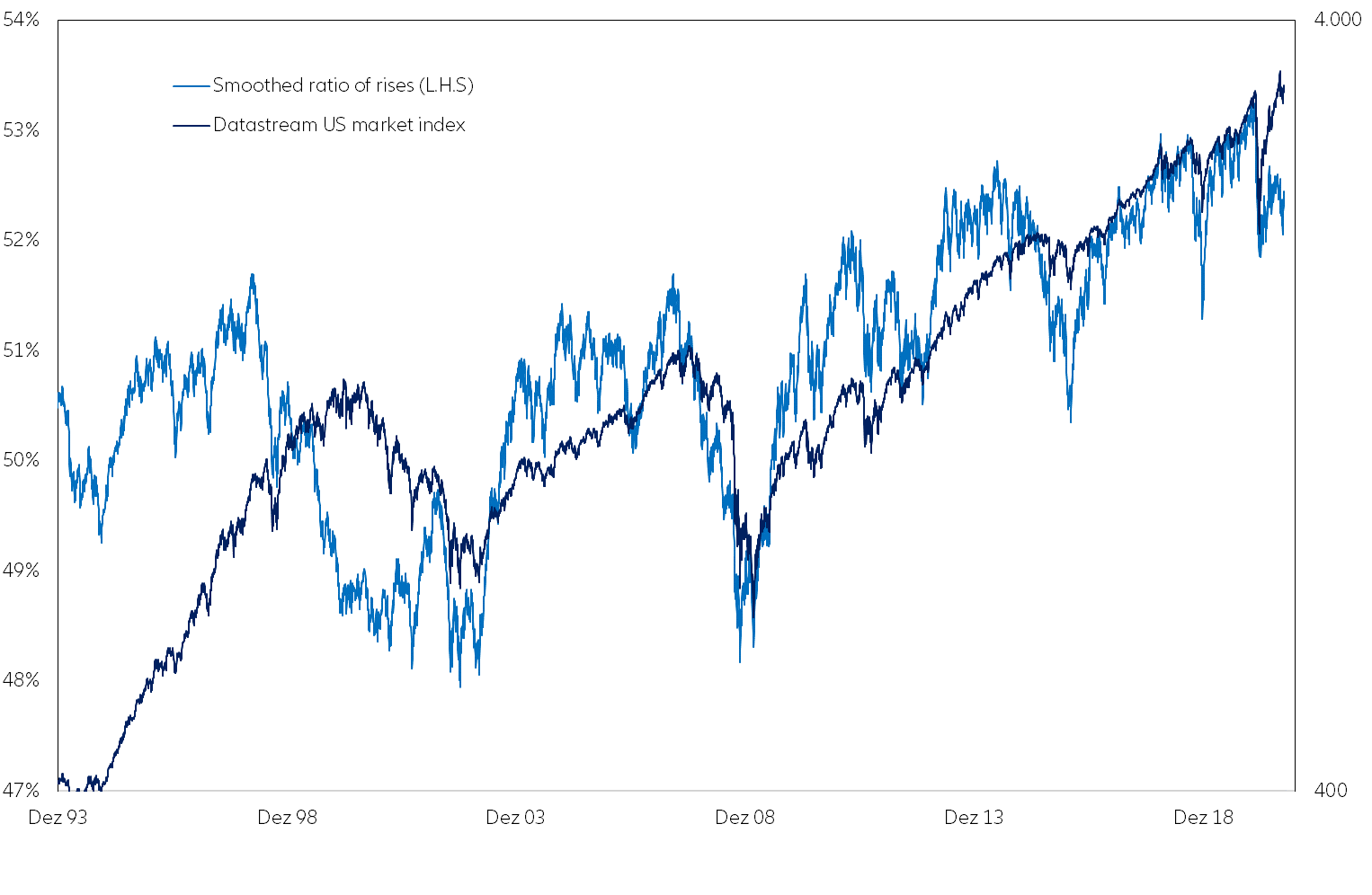

A second measure of concentration is the number of stocks that rise or fall during each trading day, the assumption being that the larger the number of rising stocks, the healthier is the market rally, for the more balanced is growth. Zooming in on the most recent period shows that the smoothed rises-to-fall ratio reached a peak on 17 January 2020.

Unfortunately, the number of rising or falling stocks varies a lot from one day to the next (as well as the number of shares that remain unchanged). Therefore, to extract a signal from the noise, one needs to smooth the

daily rises-to-falls ratio by means of an exponential average, as shown in

Figure 2 (with a daily coefficient of 0.003).

While the rally that started on 23 March has pushed the capitalization-weighted S&P 500 to new highs, the rises-to-falls ratio has failed to reach a new high. This second divergence indicates that the rally triggered by the U.S. Federal Reserve’s intervention has been a concentrated one, too. One can also observe that, at its current level of 52.44, the ratio of rises-to-falls still lies close to the upper limit of its historical range of fluctuations, that is, well above the troughs experienced in 2002 and 2008, or even in 2015.

Figure 2 – Ratio of rises-to-falls and S&P 500

How to explain the rising trend of the rises-to-fall ratio since 2008 is a question that we shall leave unanswered, at least for the time being. It may reflect the performance of the U.S. economy during that period. It may also reflect the moral hazard fostered by the Fed’s quantitative easing and forward guidance.

Intuition suggests that if the largest constituents outperform the rest of the market, that is, if their share of the market capitalization increases, concentration should be increasing. Measuring this kind of effect is precisely what a statistical metric known as entropy does.

The six-month old divergence between a rising capitalization-weighted S&P 500 and a stagnating rises-to-falls ratio is indicative of a concentrated equity market upswing. But it does not measure how concentrated this upswing has been. This is because, by design, it neglects the size of the stocks that rise or fall.

Entropy was first developed by Claude Shannon in the context of information theory, but it can easily be used to measure concentration within a stock market index. The idea underpinning entropy is a very simple one: the less frequent a signal (e.g. a letter in a text, a note in a tune), the more information it contains. Let us consider three signals with respective frequencies of 1/2, 1/4 and 1/8.

As we have

as one unit of information, signals that happen with the respective frequencies of 1/4 and 1/8 contain respectively twice and thrice as much information as a signal that happens with a frequency of 1/2. Hence, the entropy of a distribution reads as

which means that the smaller the frequencies fi, the higher the entropy. Put differently, the lower the entropy of a distribution, the higher its concentration around a few outcomes. Maximum concentration corresponds to zero entropy. It is this very observation which justifies using entropy to measure the concentration within a stock market index. To do that, one just needs to substitutes weights wi for frequencies fi and write

Using the function log500Wi

![]()

instead of the function log2Wi

![]()

ensures that if all the 500 constituents in the S&P 500 were equally weighted, its entropy would equal one, since

If we used log2〖w_i 〗, the entropy of the equally-weighted S&P 500 would equal 8.97, which is less of an appealing number to set a reference point.

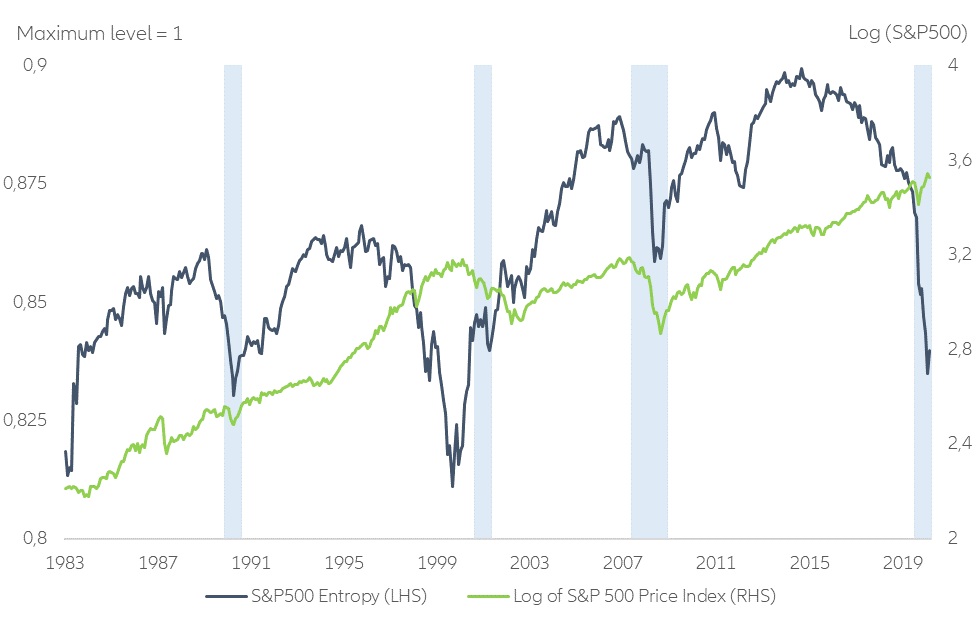

As shown in Figures 3 and 4, after slowly falling from April 2015 onwards, the entropy of the S&P 500 has dramatically fallen (i.e. its concentration has dramatically increased) since 24 February 2020 and, unlike the first two indicators that we have examined, has continued to point to increasing concentration beyond 23 March 2020.

It is now close to the record low level reached in 2000. Figure 3 also shows that entropy is much less volatile than the rises-to-falls ratio. It also shows that, like the rises-to-falls ratio, entropy tends to go south some time before the market does.

Figure 3 – S&P 500 Entropy since 1983 (shaded areas represent recessions)

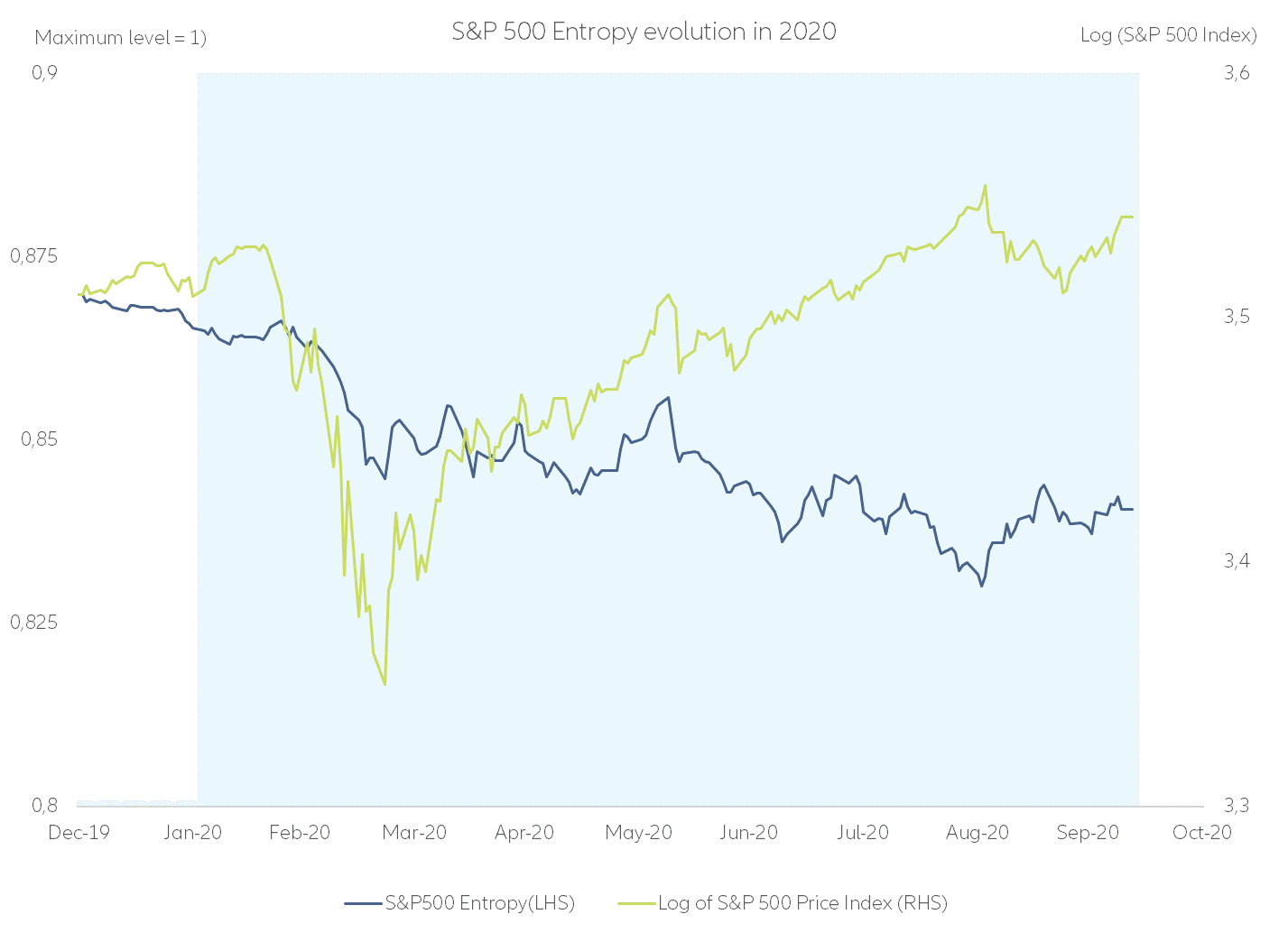

Figure 4 – S&P 500 Entropy in 2020

A zoom on the very last observations in Figure 4 shows a contrast between the February-March 2020 correction and the one that may have started

in early September. While entropy fell at an accelerating pace from

24 February 2020 to 01 September 2020, it has slightly risen since then.

The reason behind this recent rise in concentration is no mystery. The five largest stocks in the S&P 500 – Apple, Amazon, Microsoft, Facebook and Alphabet - have so strongly outperformed the broader market that their combined market capitalization has jumped by 9pp from 15% in late September 2019 to almost 24% 11 months later. During the five previous years, their combined market capitalization had only increased by 7pp. Two factors seem to have contributed to this recent increase in concentration: first, the easing of monetary policy that started in July 2019; second, the Covid-19 crisis, which pushed monetary easing further, while at the same time validating the business models of these large stocks.

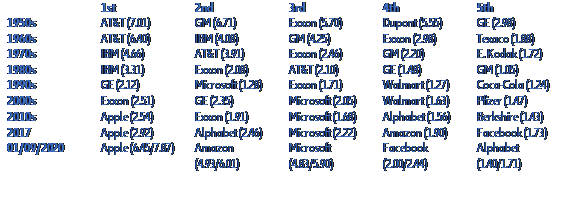

This being said, even the most brilliant narrative has a fair price. A look at Table 1 shows that good stories have changed over time. Gone are the times when AT&T, GM, IBM, GE were on the top of the world. Yet, when they were, they looked invincible and invulnerable. This is something to bear in mind as policymakers and regulators, both in the U.S. and in Europe, look increasingly intent on curbing the market power of Big Tech.

Table 1 - The five largest U.S stock by market capitalization (figures between brackets are the share of total market capitalization/S&P market capitalization)