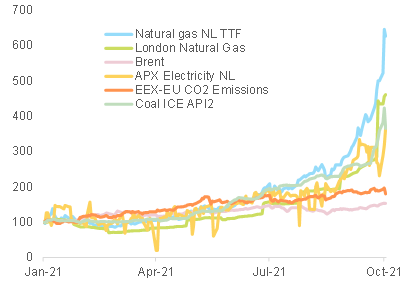

Pent-up demand, tight supply, green policy and bad timing are the recipe for skyrocketing energy prices, which could take three to six months to cool down. Europe is particularly at risk due to low stocks and its high dependence on natural gas. In recent weeks, energy prices and especially natural gas prices have surged sharply (see Figure 1), prompting countries to reactivate coal-fired electricity generation. This has caused carbon prices to spike in turn.

Figure 1 – Energy prices (January 2021 = 100)

Sources: Refinitiv, Euler Hermes, Allianz Research

The shock comes from a combination of demand and supply factors. From a demand perspective, the strong global recovery is pushing up demand for electricity and fuels. Moreover, after a quite severe winter 2020/2021 in the Northern hemisphere, inventories of liquefied natural gas (LNG) were left at low levels and now countries are rushing to restock in order to prepare for colder weather. To add to this, China has also decided to implement new environmental regulations that have further raised demand and encouraged firms to stock up on LNG.

On the supply side, in the US, about 40% of gas supply had been taken out in the aftermath of hurricanes. Although Russia has been fullfiling its contractual obligations on its long-term agreements, it has been keeping a lid on exports because it needs to restock massively for winter before increasing supply to global markets (see Figure 2). And global trade remains constrained due to limited shipping and port capacities across the globe.

Figure 2 – Russia gas inventories (BCM)

Sources: Gazprom, Bloomberg, Euler Hermes, Allianz Research

Compounding the problem are several adverse events occurring at the same time:

- Some nuclear plants are under maintenance in the UK and Germany.

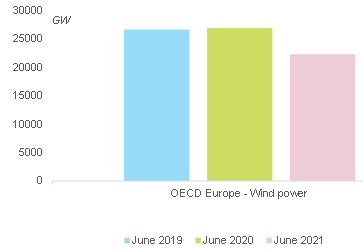

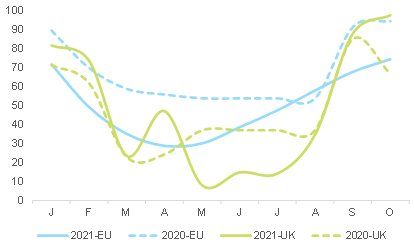

- Europe is seeing lower wind power generation (see Figure 3), leaving countries such as the UK or Spain short of several GW of power.

- In Brazil, rivers are at extremely low levels, which is a disaster for hydropower generation.

Figure 3 – Wind power generation in Europe

Sources: IEA, Euler Hermes, Allianz Research

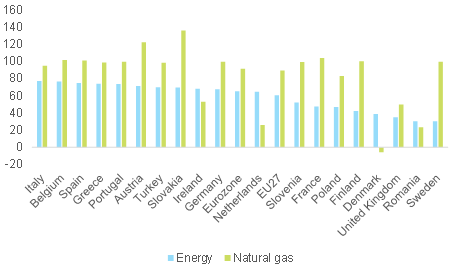

Europe is losing the bidding war and late to restocking. Surging natural gas prices are a particularly big challenge for Europe as the region depends heavily on imports (see Figure 4). But Asian countries, which lack the EU’s pipeline supplies and are thus desperate to restock, have been winning the bidding war on LNG shipments. China in particular appears willing to stock up on gas “no matter the cost”. Consequently, while many non-EU countries have managed to recover stocks levels close to Q3 2020 or even higher in the case of UK, the EU is still 25pp below full storage capacity (see Figure 5).

Figure 4 – Share of imports in consumption for energy and gas

Sources: Eurostat, Euler Hermes, Allianz Research

Figure 5 – Gas storage filling for the EU and the UK (%)

Sources: GIE-AGSI, Euler Hermes, Allianz Research

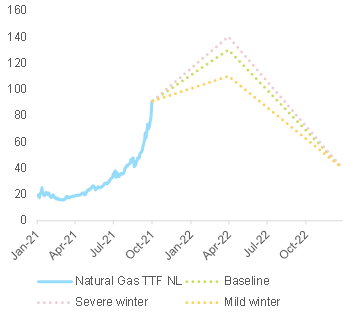

We expect natural gas prices to peak by spring 2022 in a range between EUR110 and EUR130 (Natural Gas TTF NL 1st Future Monthly), depending on the intensity of winter. Should it be very cold in the Northern hemisphere, we could see further temporary surges on energy commodities and power markets. But even if the winter is mild, countries could be inclined to restock as a precautionary measure. Overall, we believe demand should remain strong until spring 2022. In the US, the Energy Information Agency already forecasts a sharp increase of propane demand this winter, especially in the Midwest. From a supply perspective, Nord Stream 2, even if approved swiftly, would take at least four to five months to ramp up towards significant capacity. The phasing out of OPEC quotas will also provide downward pressure to energy commodities but will only be (almost) complete by May 2022. In addition, China has recently decided to restart some coalmines, but again reserves will replenish at a slow pace.

Figure 6 – Natural gas price forecast (euros)

Sources: Refinitiv, Euler Hermes, Allianz Research

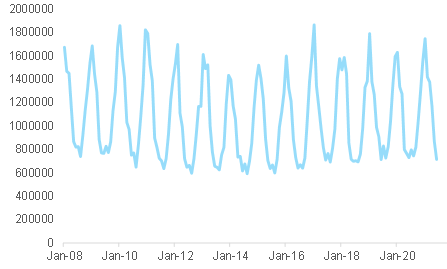

Nevertheless, we do not expect a prolonged energy crisis, mostly because supply will eventually normalize and, most importantly, in most areas demand is seasonal and will fall in the spring. In Europe, for instance, natural gas consumption decreases sharply each year in April (see Figure 7).

Figure 7 – Natural gas consumption in the EU (terajoule)

Sources: Refinitiv, Euler Hermes, Allianz Research

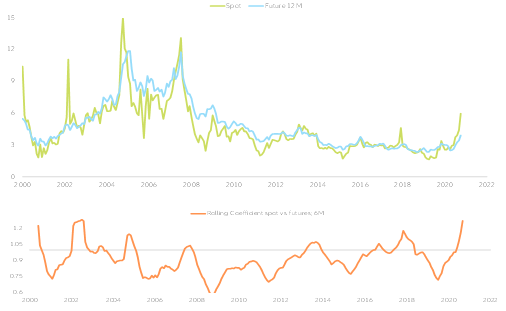

The futures market is also pointing towards a price consolidation: The current spot price for gas has decoupled from market expectations 12 months from now. In other words, markets are in a strong backwardation mode and suggest a normalization starting in Q2 2022 by about 30% (see Figure 8).

Figure 8 – Natural gas spot, futures and cross-correlation

Sources: Refinitiv, Euler Hermes, Allianz Research

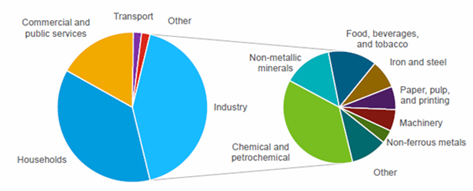

While we do not expect any disruption in industries, the energy sector could see higher insolvency risk, especially in the UK but also in Germany. In the EU, natural gas is mostly consumed by industry and households (see Figure 9). From a sector point of view, some segments of manufacturing such as food, paper, chemicals, metals or refining activities are quite energy-intensive and large consumers of natural gas. Based on our previous research on European firms’ pricing power , refined oil products and the food sector should remain rather immune to current developments. They have improved profitability in recent years and have sufficient pricing power to offset higher input prices. Iron and steel should also fare quite well as their end market should prove resilient. Eurozone automotive manufacturers have regained pricing power, thanks to the chip shortage and could pass on higher prices and the construction sector also benefits from strong pricing power.

Figure 9 – Breakdown of final natural gas consumption in the EU

Sources: Eurostat, Euler Hermes, Allianz Research

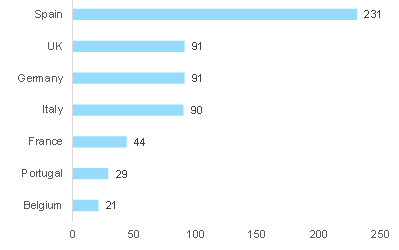

However, small utility companies have already seen financial stress, particularly in the UK. In a very fragmented market (see Figure 10), a number of small UK distribution companies, which buy power on the wholesale market and sell it to final clients but did not hedge their supply while offering guaranteed low prices to customers, have requested government support. As the government has refused to act, some will likely go bust. In a normal year, about seven to eight power distribution companies file for bankruptcy in the UK; as of October 2021, eight have already done so and the count will likely go higher. However, this situation is not a direct consequence of fragmentation. Other markets are also very fragmented but market participants are managed more responsibly, have the ability to pass on price increases and/or are under a tighter regulatory framework. For example, in Spain, although the market is highly concentrated and there are many small local actors, because most consumers are on dynamic contracts (which allows for daily price revision), they are not in the same situation as small distributors in the UK.

Germany’s market structure is similar to that of the UK’s as it chose to liberalize the energy sector in order to create choice for consumers and dismantle monopolies. In addition, there are no utility price caps in Germany and households buy energy in a mostly unsupervised market. As power futures are at very high levels, some distributers and suppliers with fragile cash positions could run into liquidity issues or even become insolvent in the coming months. And as in the case of UK, firms will not be able to rely on policy support: Recently the Bundesnetzagentur (BNetzA), the German energy regulator, said it was not its role to monitor procurement strategies or pricing mechanisms.

Figure 10 – Power suppliers by countries (2018)

Sources: Vlados et al. (2019), Euler Hermes, Allianz Research

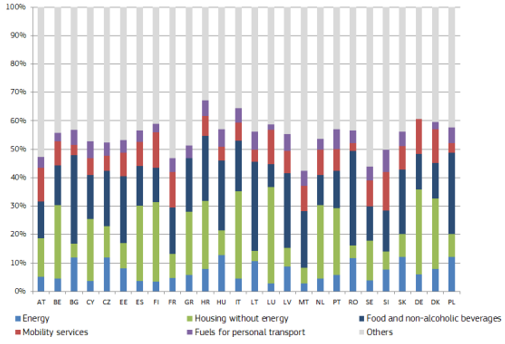

Households will take most of the hit from higher energy prices, and France, Italy and Spain are firefighting with strong support. While households in Germany and Eastern European spend more on energy than those in France, Italy or Spain (see Figure 11), higher prices pose a problem for poorer households across the EU. According to the

European Commission, on average in the EU, the lowest income decile households spent 8.3% of their revenues on energy in 2018, while middle-income decile households spent only 6.3%. Higher energy prices also pose an inflationary risk as the energy component accounts for almost 11% of CPI in Germany and Spain and about 9% in the Eurozone HICP.

Figure 11 – Breakdown of household consumption in Europe

Sources: European Commission – DG ENER, Euler Hermes, Allianz Research

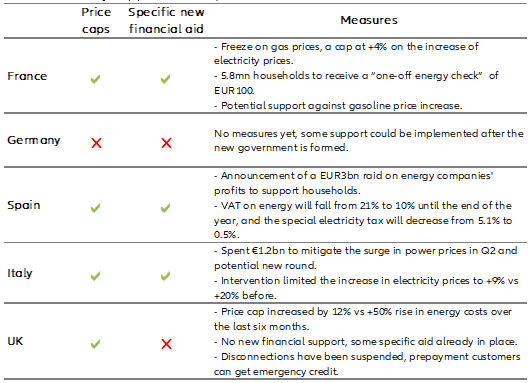

In response, France, Italy and Spain are reacting strongly with policy support as the matter is socially sensitive (see Table 1). The UK and Germany have not reacted as strongly, though in the latter support measures could be implemented after the new government is formed.

Table 1 – Policy support in Europe

Source: Euler Hermes, Allianz Research

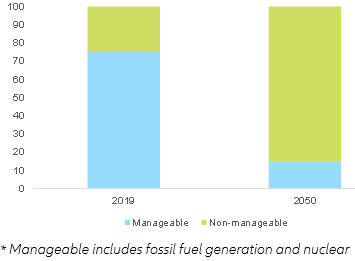

The current crisis could create political momentum for reforming the EU energy market and designing an energy strategy for Europe via markets and/or strategic alliances, especially as the green transition will create rising volatility in energy markets. According to IRENA, electricity production needs to double to support the green transition and renewables need to grow substantially to meet greenhouse gas reduction targets (see Figure 12). Nevertheless, renewable energies are electricity-generation sources that are difficult to manage as smart grids and storage capacities are still inadequate and the current approach is to install overcapacities and use curtailment to match grid demand. As climate change could make extreme weather events more frequent and could change long-term wind cycles, we should expect more volatility in power supply in the future. This speaks for the need of huge investments in the necessary infrastructure; in particular, sector coupling is a promising path to tackle the storage problem. In the meantime, however, in case of frequent power crunches, should carbon prices remain relatively low, we could even see setbacks in terms of greenhouse gas emission targets as electricity producers would switch to coal or oil – what we see happening today. This could be even more acute as Europe has been underinvesting in natural gas facilities despite natural gas being the fossil fuel with the lowest carbon footprint.

Figure 12 – Electricity generation by type (%)

Sources: IRENA, Euler Hermes, Allianz Research

France and Spain both back an overhall of European electricity markets by revamping the marginal system, which pegs the next day's final power price to the most expensive fuel needed to meet anticipated demand. This should help crack down on speculation and ensure greater accuracy in pricing. Spain has also demanded a common EU approach, including natural gas purchases to counteract vendors’ market power and the building of strategic reserves. Luxembourg and France also back a possible return to long-term gas supply contracts to ensure price stability, which would demand a shift in the Commission's current policy.

European countries made the mistake of thinking that pipelines alone were sufficient to secure gas supply from Russia. Yet, the recent months have shown that countries with strong strategic vision and purchasing power were able to squeeze Europe out of supply. In order to avoid future energy crises and resorting repeatedly to emergency spending to support households, Europe needs to design and implement a proper energy strategy. This could be done using market instruments to hedge price volatility and secure supply or by making strategic alliances with large exporting countries such as Russia, Qatar, Australia or the US.

Author

Sector Advisor