This IFrame contains external resources. The provider may be collecting information about your interaction with this content by using cookies and may use this for targeting their offers. Please accept cookies in order to show the IFrame.

Executive Summary

Vaccine security will shape the grand reopening. While advanced economies delivered on immunization campaigns, vaccine hesitancy and second-generation vaccines are first-order priorities. In the meantime, under-vaccination in Asia and in Emerging Markets may cause desynchronized growth paths.

A multifaceted recovery: high-pressure economics in the US, low-pressure economics in Europe. We expect global GDP to grow by +5.5% in 2021, with the US being a clear outperformer. In Europe, the return to pre-crisis levels will take one year more compared to the US (Q1 2022) and the return to the pre-Covid-19 growth path an extra four years – if it happens at all.

Revenge spending is happening but residual savings to amount to EUR500bn in Europe, and USD1trn in the US. Consumption will lead the recovery as we expect pent-up demand to reach 3% of GDP in the US and the UK, and around 1.5% of GDP in Europe. However, hoarding behaviors remain for precautionary reasons, complicating policy choices down the road.

Inflation, what inflation? Bottlenecks in terms of supply (raw materials, transportation capacity, workers) will likely keep cost inflation at a five-year high until the end of 2021. Companies’ pricing power remains limited, notably in Europe. Households’ purchasing power will be under pressure as the employment gap (4 million jobs in the Eurozone and more than 7 million in the US) will keep wage inflation in check. But no monetary inflation is likely as the velocity of money is at a record low.

The Faustian pact between expansionary fiscal and monetary policies is here to stay. We expect central banks to be patient before hiking rates in 2023 (some exceptions: Norway, New Zealand, the UK by September 2022). Total global debt increased by more than USD24trn in 2020, including USD12trn of public debt and USD12trn of private debt. Emerging Markets are more exposed to a sudden shift in market sentiment, which would impose a disorderly adjustment of currencies and debt.

Political crossroads ahead for Europe but no repeat of the 2012 crisis in 2022. In the Eurozone the Next Generation EU fund and the ECB will support the recovery and keep financial stress at bay while German-French elections may create policy surprises. Yet, watch out for heterogeneity.

Credit risk under control. The insolvency puzzle continues as corporate debt increased to new highs but cash on the balance sheet did, too, and liquidity support to firms will continue into 2022. European non-financial companies will have to increase their margins by 1.5pp on average in order to make their debt sustainable.

Green is the new black of industrial policy. The transition towards a cleaner model of growth will require the definition of a real new industrial policy, consisting of generating new fiscal resources, subsidizing the transition, protecting domestic producers and investing in infrastructure. Over the 2021-50 period, annual energy sector investment has to increase by around 1% of global GDP compared to today's levels to enable a net-zero energy transition. With USD1.3trn, investment in renewable electricity will need to surpass the highest level ever spent on fossil fuel supply (USD1.2trn in 2014).

Political risk remains amid a new US paternalism and tactical multilateralism. The US has launched a new wave of global and multilateral initiatives for climate change and tax policies. But such a revival in international engagement does not necessarily mean unselective multilateralism: so far in 2021, the US has been the most active with trade protectionist measures and China and Germany the most targeted (in net terms). While the Asia-Pacific region could see some acceleration in the expansion and implementation of free trade agreements (eg. RCEP, CPTPP etc.), it is not immune to pre-existing geopolitical tensions that have worsened with the Covid-19 crisis (eg. China and the “Quad”).

Markets’ risk-on music keeps on playing but mind endogenous financial instabilities. Most asset classes are front-running the grand reopening and strong policy support far better than expected. But the upside is limited now while growing imbalances increase risks to the downside.

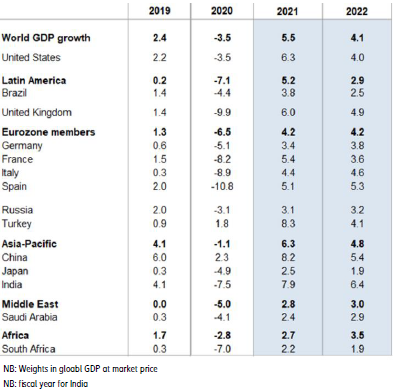

Figure 1: Real GDP growth forecasts, %

Sources: Euler Hermes, Allianz Research

A grand reopening, but a multifaceted recovery

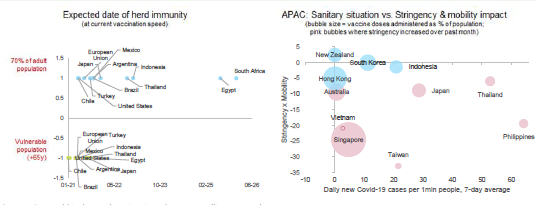

A grand reopening, but a multifaceted recoveryVaccine security to shape grand reopening. While advanced economies delivered on immunization campaigns, vaccine hesitancy, and second-generation vaccines, are first-order priorities. However, avoiding the vaccination fatigue trap will be key for a sustainable reopening as demand-side hurdles are now following the supply-side ones. In the meantime, under-vaccination in Asia and in Emerging Markets may cause desynchronized growth paths. Stop-and-go government strategies to cope with the increase in new cases – albeit more moderate than previous waves - are still likely to continue.

Figure 2: Covid-19 sanitary and vaccination situation

Sources: Euler Hermes, Allianz Research

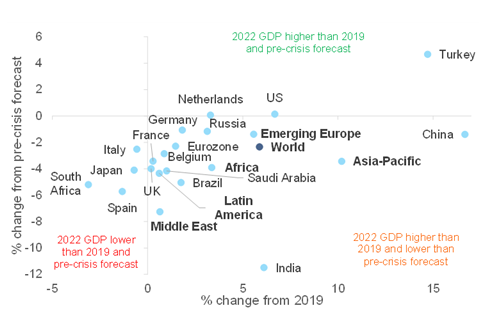

Multifaceted recovery. High-pressure economics in the US, low-pressure economics in Europe. After nearing pre-crisis levels of growth in Q1 2021, fueled by the US and China, the global economy looks set for a strong mechanical recovery in the coming quarters amidst a grand reopening in several advanced economies. We expect global GDP to grow by +5.5% in 2021, with the US being a clear outperformer and the only economy where growth will exceed its pre-Covid-19 path from the end of the year. In Europe, the return to pre-crisis levels will take one year more compared to the US (Q1 2022) and the return to the pre-Covid-19 growth path an extra four years – if it happens at all.

Global trade is set to rebound strongly in 2021, but bottlenecks will lead to short-term hurdles. We forecast growth of +7.7% in volume terms (after -8.0% in 2020) and +15.9% in value terms (after -9.9% in 2020), supported by favorable base effects, a stronger-than-expected momentum in the first months of the year and expectations of robust exports out of Asia-Pacific, as well as strong imports in the US, Europe and China. Indeed, the global exports rebound has until now clearly been driven by the Asia-Pacific region, with exports from most other regions still below pre-crisis averages. However, the global supply-demand imbalance could be exacerbated during the summer, given new Covid-19 outbreaks in Asia-Pacific, notably in Taiwan, on which the world has become increasingly dependent in the electronics sector. The impact of these outbreaks on trade volume is likely to be temporary and limited to Q2 (after which the epidemics in Asia-Pacific trade hubs should be controlled), while high prices due to input shortages are likely to remain for most of this year.

Revenge spending is happening but residual savings to amount to EUR500bn in Europe, and USD1trn in the US. The grand reopening sets the stage for a V-shaped recovery, but global supply still needs to catch up. We estimate pent-up consumption at 3% of GDP in the US and UK in 2021, and at around 1.5% in most European countries. Consumption will lead the recovery but hoarding behaviors remain for precautionary reasons, complicating policy choices down the road. At the same time, global supply chains remain disrupted, with suppliers’ delivery times and container prices from Asia at record highs. As effects from fiscal stimuli will start to be even more visible in the US as well as in the Eurozone in the coming months, demand for goods will remain high (notably for building materials and semiconductors), bringing input prices to a record high during the summer. This situation is likely to prevail until the end of the year before demand starts normalizing and production capacity ramps up, thanks to upcoming business investments. The key question will remain companies’ pricing power capacity, which is limited, notably in Europe .

Figure 3: 2022 GDP, compared to 2019 and pre-crisis forecast

Sources: Various, Euler Hermes, Allianz Research

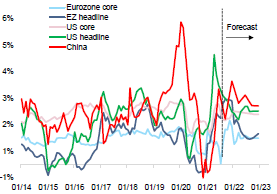

Inflation, what inflation? Bottlenecks in terms of supply (raw materials, transportation capacity, workers) will likely keep cost inflation at a five-year high until the end of 2021. Global inflationary pressures are at record high levels but the good news is that they are mainly driven by energy prices and USD appreciation, which should prove temporary. The cost inflation is likely to prevail until 2022, when pressures from labor shortages should reduce along with the rise in input and asset prices. Competition to access the workforce will significantly intensify with the grand reopening. The time needed for the reallocation of the workforce, the lower incentive to work in the immediate aftermath of the reopening (relief effect) and the persistence of high social transfers could weigh on the pace of the job market’s recovery as mirrored by disappointing numbers of non-farm US payrolls in April. In the UK, job shortages have continued to intensify since the second stage of eased restrictions in April, notably in the transportation, construction and catering and hospitality sectors. In the medium-run, negative output gaps should keep wage pressure in check as well as the employment gap compared to the long-term average (4 million jobs in the Eurozone and more than 7 million in the US). In addition, companies have limited pricing power, notably in Europe. Finally, there is no monetary inflation as the velocity of money is at a record low.

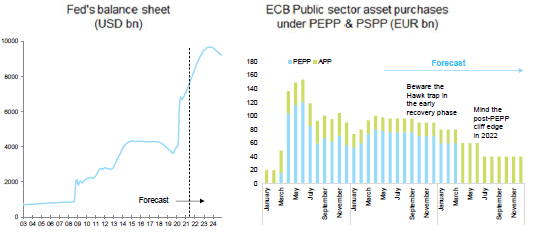

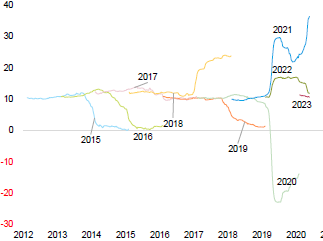

Faustian pact between expansionary fiscal and monetary policies to stay. In the short-term, central banks will continue remaining highly accommodative (with some exemptions such as Norway, New Zealand and the UK by September 2022). The Fed is expected to deploy some elements of language on tapering starting next year, with an operation twist from Q2 2022 and then a gradual reduction in securities purchases from USD120bn per month to 0 in H2 2023, followed by a first rate hike in H2 2023. The ECB will continue to ensure favorable financing conditions during the early phase of the recovery even as Eurozone inflation is likely to overshoot at 2.5% y/y in H2 2021. Ideally, it should move away from pre-committing to a quarterly purchase pace in an effort to make full use of PEPP’s inherent flexibility. From September onwards, the ECB should start to give more guidance on what “life after PEPP” will look like. In particular, the focus will shift to the management of the PEPP cliff-edge when the programs end in March 2022. The monthly asset purchases under the APP will most likely have to be lifted – at least for a few months – to EUR40-60bn to continue to ensure favorable financing conditions. However, this could see the ECB run into German debt limits: We calculate that EUR40-60bn in monthly APP purchases would only allow for the APP to continue for seven to 10 months after March 2022. As we have learnt in the past, the ECB tends to have another trick up its sleeve i.e. limits can be moved. In that regard, the results of the ongoing ECB strategy review expected in September could come as a game-changer, including by rolling over PEPP’s flexibility to APP. Some Emerging Markets should be an exception against rising imported inflation as protection of real household purchasing power will remain the focus in an environment of increasing middle-income traps and social risk. Brazil, Romania, Czechia, South Africa and Nigeria are likely to hike three times by mid-2022.

Figure 4: Inflation forecasts

Sources : Refinitiv, Euler Hermes, Allianz Research

Figure 5: Fed & ECB scenarios

Sources : Refinitiv, Euler Hermes, Allianz Research

Political crossroads ahead for Europe but no repeat of the 2012 crisis in 2022. Europe has learned from its crisis mistakes of the past, so don’t expect to see any active fiscal or monetary tightening before H2 2022. In fact, the Next Generation EU fund, next to providing a GDP boost of +1pp in 2021, will also cushion fiscal consolidation needs with grants not included in national deficit calculations. Meanwhile the ECB will look through the temporary inflation overshoot and focus on maintaining favorable financing conditions, closing spreads (i.e. Italian fiscal heterogeneity will be managed) and boosting policy room for maneuvering via the strategy review as German debt limits are moving closer. Among the large EU countries, Italy will stretch its national fiscal space the most (public deficit of 11.8% and 5.8% of GDP in 2021 and 2022) and, at the same time, will receive by far the largest share from the EU Recovery Fund (EUR192bn, of which EUR69bn in grants). The prospect of a lasting fiscal integration in the EU therefore depends on the success of the Italian recovery plan. If the implementation is effective, Italy could indeed regain political credibility in the eyes of the "frugal" sceptics. Capital markets have yet been complacent with Italy’s aggressive fiscal policy. The 10y spread over Germany has stabilized in a range of 110 to 90bp. With ECB purchases, fiscal variables have indeed lost much of their explanatory power for spread movements; a dangerous spread-widening is only likely if the “Draghi put” expires and political risk (“Italexit”) reappears. In this context, the general elections of H1 2023 are the next decisive event. Factoring in national elections in other key political heavyweights Germany (Base case: CDU/Green party coalition) and France will keep a lid on EU integration momentum until spring 2022 while thereafter we expect to see more evolution (investment in green & digital) than revolution. In France, on the one hand, to avoid any social discontent, we do not expect the government to implement any ambitious and controversial reforms until the elections. On the other hand, President Macron will also need to reassure the electorate regarding pre-Covid commitments such as the pension reform that it still qualifies as an “absolute necessity”. In this context, there is a slim chance that the government pushes for a softened version of the reform that is likely to trigger protests and social unrest again.

Herd policymaking: interventionism will still be at work in 2021. Switching from short-term to long-term policy will be gradual, and a complete withdrawal can take up to one year. Removing state support means a higher risk of policy mistakes, especially as in theory firms still hold high cash balances, which might tempt some policymakers to withdraw assistance mechanisms faster. The increase in cash balances of non-financial companies as of April 2021 was EUR180bn in France, EUR169bn in the UK, EUR 95bn in Germany and EUR81bn in Italy. However, this cash should finance the recovery (i.e. stocks and WCR) and the new investment cycle, not a deleveraging process.

Avoiding the mistakes of an early or disorderly fiscal tightening will be key for the sustainability of the recovery. China is already engaged in reducing its monetary and fiscal impulses and other countries could be tempted to follow suit. However, terminating assistance mechanisms in a premature manner could, for example, be the trigger of a new wave of insolvencies among non-financial companies. Bringing long-term perspectives to the corporate sector with infrastructure projects and clearly defined industrial policies could restore confidence and liberate excess cash in the corporate sector. In the UK, for example, the phase-out of policy support measures is set to take a full year. The furlough scheme ends in September 2021 though the reopening started in April. Meanwhile, the state-guaranteed recovery loan scheme ends in December 2021, all the discounted business rates end in March 2022, the reduced VAT rate ends in April 2022 and the state-guaranteed mortgage loan scheme ends in December 2022.

An asymmetric normalization of credit risk across sectors. Massive state interventions helped suppress a significant wave of insolvencies in 2020, with the year ending with a -12% drop globally rather than a +40% surge (ceteris paribus estimation). We expect a pragmatic and fine-tuned phasing-out of support measures in order to manage the pressure on companies’ liquidity and solvability. Indeed, cash on balance sheets increased to new highs at a global level but so did corporate debt. This will command European non-financial companies to increase their operating margins to keep their debt sustainable (by 1.5pp on average, everything else being equal). In addition, the sectorial asymmetry of the shock led to wide heterogeneity across sectors in terms of revenue, profits and impact on balance sheets. De facto, credit risk ratings recorded a stronger hit in sectors that bore the brunt of social and mobility restrictions, such as hotels and restaurants and transportation, with substantial positive performance conversely in chemicals, pharmaceuticals, retail and agrifood. The V-shaped global recovery will lead to a rebalancing in credit ratings from the wave of deteriorations posted in 2020 but the heterogeneity across sectors is likely to prevail until 2023.

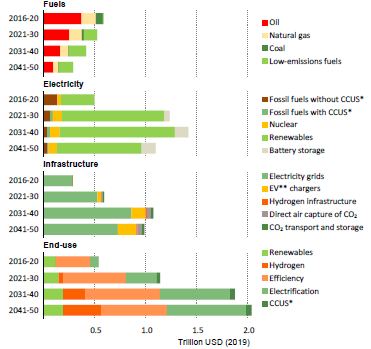

The global economy could spontaneously converge toward a new Marshall plan for a climate-friendly recovery. We calculate that the USD2.3trn infrastructure package has the potential to maintain the US economy’s growth potential at close to +2% by 2030 instead of +1.4% without it. However, execution risk could pose a problem for the EU EUR750bn Recovery Fund. Accompanying demand over the medium-term will be key in order to liberate excess savings not consumed via pent-up demand. Around 40% of the excess cash from households and companies (currently at more than 10% of GDP in both the US and Europe) will morph into spending by year-end, thanks to high pent-up demand. The unleashing of the 60% remaining will depend on the size of a positive confidence shock that only a long-term, massive and coordinated fiscal plan can initiate. In the IEA projections (Figure 5), for a net-zero emission compatible transition, investments need to increase rapidly in electricity generation, infrastructure and end-use sectors while fossil fuel investment drops sharply.

Figure 6: Projected global average annual energy investment needs for the net-zero energy transition.

Source: International Energy Agency (2021), Net Zero by 2050, IEA, Paris: Net Zero by 2050 Scenario. *CCUS: Carbon capture, utilization and storage; **EV: Electric vehicle.

In particular, annual investment in electricity generation would need to increase from about USD0.5trn to USD1.6trn in 2030. The USD1.3trn of investment in renewable electricity is in the range of the highest level ever spent on fossil fuel supply (USD1.2trn in 2014). Energy infrastructure should increase from around USD290bn to USD880bn in 2030 and include electricity networks, public electric vehicle (EV) charging stations, hydrogen refueling stations and import and export terminals, direct air capture and CO2 pipelines and storage facilities. Investments in end-use sectors should rise from USD530bn to USD1.7trn in 2030 and include spending on deep retrofitting of buildings, transformation of industrial processes and the purchase of new low-emissions vehicles and more efficient appliances.

Besides supporting demand, large infrastructure projects will define new industrial policies with similarities across countries, pushing via innovation and subventions towards cleaner energy models, fostering digitization. They will not only maintain a high level of protectionism, but also result in more coordination at a global level in terms of tax policy, using multilateralism and climate policy as a tactical tool of domination by the law. The US will be at the forefront of what we could consider as a new form of paternalism. Disclosure can play an important role in fostering protectionism as supply chain laws coupled with ESG KPIs that, for instance, include labor and human rights, result in diverging investment flows away from foreign “red-flagged” activities into domestic ESG overperformers.

Political risk remains with a form of US paternalism and tactical multilateralism. Joe Biden’s foreign policy marks a revival of large-scale multilateral initiatives such as the organization of a virtual two-day climate summit in April 2021 or the proposal of a global minimum corporate tax rate of 15%. This approach, which could be compared with a form of paternalism or a leadership by the law or norms, initiates in our view a form of tactical multilateralism. In the case of the tax initiative, there is a strong need to find new fiscal resources. Total global debt has increased by more than USD24trn between Q4 2019 and Q4 2020, including USD12trn of public debt and USD12trn of private debt. USD10trn of supplementary debt is expected to be issued in 2021. The need to find new sources of fiscal revenues will imply not only raised taxes at a domestic level but also at an international level. In terms of climate change policy, a leadership position will offer the possibility to impose new norms (of trade among others) internationally.

Such a revival in international engagement indeed does not necessarily mean unselective multilateralism. Indeed, trade protectionist measures are still being implemented in 2021, with the US being the most active and China and Germany the most targeted (in net terms). Regulation affecting digital commerce is also becoming increasingly apparent at the global level. While the Asia-Pacific region could see some acceleration in the expansion and implementation of free trade agreements (e.g. RCEP, CPTPP etc.), it is not immune to pre-existing geopolitical tensions that have worsened with the Covid-19 crisis. Notably, China’s relations with each of the Quadrilateral Security Dialogue members (the US, Australia, India and Japan) have become more tense over the past year, with trade tensions and territorial disputes. While we do not expect these issues to become economically significant in the short term, they are symptomatic of a change of dynamics in the geopolitical and global initiative spheres.

Markets have already celebrated, now they have to digest

The Fed Funds future market does not expect more than a 25bps hike in the next two years. Investors remain thus aligned with the Fed's communication to deliberately take the risk of being behind the curve. However, so far in Q2, movements in capital markets have been much more muted and contrasted than in Q1, during which a clear growth positioning took hold of all market segments. Markets have not challenged the reflation trade that dominated Q1, but they are now showing more concern about the inflation risk and the future course of monetary policy. So while the economy is gearing up for the grand reopening, capital markets are already one step ahead.

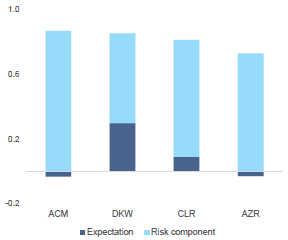

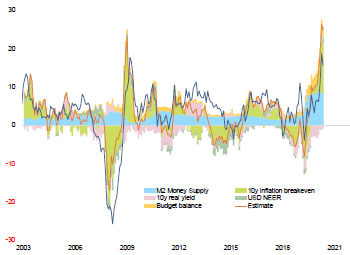

This rising uncertainty can be seen very clearly when decomposing nominal long-term US yields into their expectation and risk components (nominal term premium). Since the beginning of the year, the 60bp increase of US 10y yields is almost entirely due to the risk component (nominal term premium), reflecting heightened uncertainty about the economic and monetary equilibrium of the post-Covid era. Long-term expectations about inflation and the real equilibrium rate have so far remained anchored.

Figure 7: US 10y - breakdown of YtD increase (different term structure models*)

*Term structure models used: ACM (Adrian, Crump & Moench, 2013), DKW (D'Amico, Kim & Wei, 2018), CLR (Christensen, Lopez & Rudebusch, 2010) and AZR (proprietary Allianz Research Model)

Sources: Refinitiv, Euler Hermes, Allianz Research

Figure 8: US 10y term premium – breakdown of YtD increase (different term structure models*)

*Term structure models used: ACM (Adrian, Crump & Moench, 2013), DKW (D'Amico, Kim & Wei, 2018), CLR (Christensen, Lopez & Rudebusch, 2010) and AZR (proprietary Allianz Research Model)

Sources: Refinitiv, Euler Hermes, Allianz Research

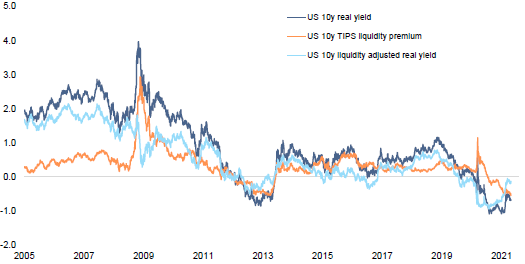

At first glance, this seems to be at odds with the development of break-even inflation, which rose by another 10bps to close to 2.5% for the 10-year maturity, pushing real yields further into negative territory (-25bp). But again, the breakdown of risk and expectation components shows that the recent rise is not due to a change of long-term expectations but to tight market conditions (liquidity risk premium). The reflation trade is becoming increasingly crowded (eg. strong inflows into TIPS ETFs) while TIPS supply is withdrawn by central bank purchases. Adjusted for the liquidity risk premium, real yields have actually recovered to pre-crisis levels, so the recovery is already fully priced in.

Figure 9: US 10y real yield – recovery fully priced in after adjusting for market frictions*

*based upon D'Amico, Kim & Wei (2018)

Sources: Refinitiv, Euler Hermes, Allianz Research

In our view, markets now have limited upside potential. Sovereign bond markets in the US but also the Eurozone have rebuilt a cushion against uncertainty. Their risk component of nominal yields is large by historical standards. The distribution of potential outcomes is skewed to the downside, especially in the US. We see only a 14% probability for the US 10y yield to finish the year above 2%. The rise of the US curve also impacted European yields and helped the Bund 10y to catch up to fair value (-0.25%). Improving economic momentum and increasing tapering rumors have also contributed. We think that a switch into positive territory could be possible (18% probability), but we would not consider it sustainable.

On the one hand, monetary and financial conditions will continue to be supportive, especially for risky assets. On the other hand, perceived inflation risk, a new global sharing of the value added, regulation and new assertive industrial policies create the potential for financial instability. Monetary aggregates show strong fluctuations as the velocity of money (the flow of “liquidity”) is far more unstable, especially in financial markets, than its quantity (the stock of “liquidity” generated by QE). Risky assets are thus not totally in a safe spot.

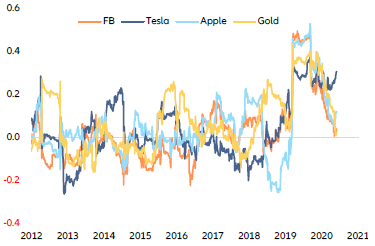

Credit spreads have remained close to the year lows, but the most interest rate-sensitive stocks or equity sectors have moved sideways or fallen. Former market darlings such as Tesla or the Ark Innovation ETF now trade close to ~35% below the year high.

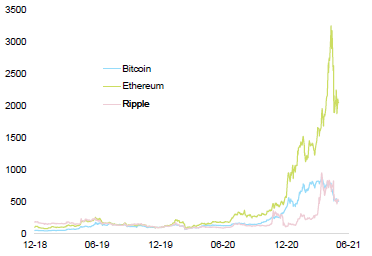

Other highly speculative plays, such as cryptocurrencies, have also taken a hit. Note that the correlation between Tesla and Bitcoin has recently increased (Figure 9). In the wake of the reflation trade, the gold sector (gold itself and gold mines) is on track to deliver double-digit returns in Q2 after posting negative returns in Q1.

Figure 10: Bitcoin correlations

Sources: Refinitiv, Allianz Research. Correlations are computed using a 6M rolling correlation on daily changes

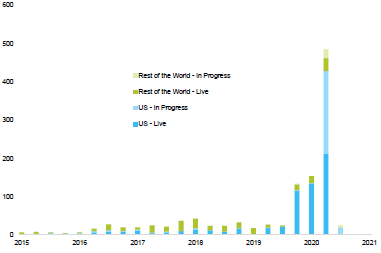

All in all, it is past midnight for risky assets! As we showed in our last quarterly publication, our Kindleberger market cycle clock keeps ticking and has now made it past midnight. The combination of extreme valuations paired with elevated levels of overtrading has led to large but isolated market corrections and is increasing the current market fragility. Among several late market cycle indicators, the rapid market correction of “new” overtraded assets, as is the case for SPACs (Special Purpose Acquisition Companies) and cryptocurrencies, have caught the eyes of many market participants.

SPAC IPOs have come to a halt in Q2 2021, leading the market to substantially correct. This comes after a substantial acceleration in both volumes and prices of this “new” financial instrument in 2020 and Q1 2021. As of today, more than 60% of the SPAC mergers that have been announced since the start of the year are now trading below the IPO price of their SPAC.

Figure 11: # of SPAC IPOs (live & in progress)

Sources: Refinitiv, Euler Hermes, Allianz Research

As for cryptocurrencies, in early Q1 2021 the aggregated market cap of cryptocurrencies skyrocketed above the USD2trn mark, only to lose more than USD500bn in a matter of days. It must be conceded that cryptocurrencies are no strangers to such sharp movements but the natural question that arises is where did this money go? Although the answer in this “new” investment is not straightforward, it confirms the recent market exuberance, overtrading and irrationality.

Figure 12: Cryptocurrencies vs USD (100 = 31.12.2019)

Sources: Refinitiv, Euler Hermes, Allianz Research

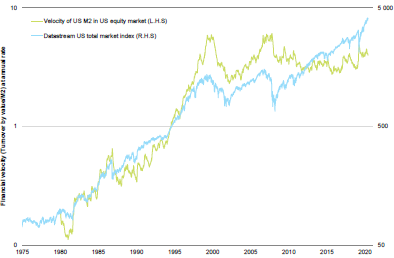

Another clear red flag that combines overtrading with increased moral hazard is the rapid increase in money velocity within financial markets. This increase is relevant as it shows that the recent equity rally has partly occurred thanks to the market’s unconditional trust in central banks’ unconditional put protection, which has, in turn, led to a rapid increase in financial money velocity. This red flag is particularly important as it is not the quantity of money but its circulation that causes asset prices to rise or fall and historical experience shows us that central banks do not control the velocity of money, especially in capital markets.

Finally, another signal of the recent market frothiness and overtrading can be found in the increasing amount of margin debt and deposits in US clearinghouses, triggered by the rapid increase in options trading volumes since March 2020. At this point, things start to take a systemic flavor and although we maintain that, at current levels, there is enough public and private liquidity in the market to absorb the increased trading volumes, it is an overtrading red flag.

Figure 13: Capital markets transactions velocity

Sources: Refinitiv, Euler Hermes, Allianz Research

On the fundamentals side, there has been a clear global frontloading of “good” earnings surprises into 2021, to the detriment of 2022 earnings expectations. This pattern can be observed across the globe and specifically in the Eurozone and Emerging Markets. Despite being a normal consequence of the strong Q1 earnings season, the grand reopening may not grant enough positive earnings tailwinds to warrant the extreme amount of frothiness and positive expectations. Because of this, the current over-stretched earnings expectations leave little to no room for further upside potential as the probability of experiencing at or below expectations earnings numbers far outpaces that of experiencing upside earnings surprises. This leaves markets in a really fragile spot and at the mercy of changes in investor sentiment.

Figure 14: S&P 500 Consensus EPS growth (in %)

Sources: IBES, Refinitiv, Euler Hermes, Allianz Research

But what does this all mean for risky assets? Despite the mounting evidence of an upcoming market clean-up/consolidation, we remain convinced that policymakers are fully aware of the situation and would backstop any sign of a full-fledged market erosion. Due to that, we expect the unplugging of key support measures to be contained and extremely gradual to allow for a mild but structural re-convergence to fundamentals. In this regard, we expect global equity markets to finish 2021 with upper single-digit returns but to converge towards long-term average returns (~5 to 7%) in 2022. In this context, we still expect the Eurozone and the UK to outperform both US and EM equities.

Figure 15: S&P 500 decomposition (in %)

Sources: Refinitiv, Euler Hermes, Allianz Research

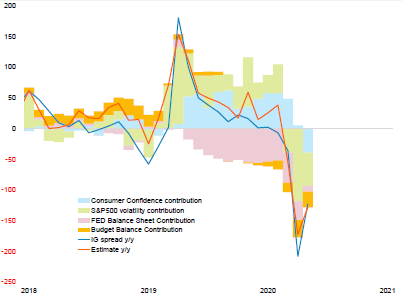

Similarly, and on the back of lax policies, credit spreads are set to range-trade for the remaining of the year while allowing for some initial market clean-up within the high yield space. Because of that, we believe investment grade credit will remain contained close to current levels until year-end while we expect some mild widening within the high-yield space due to early market consolidation. For 2022, we expect credit spreads to structurally widen at a 20 to 30bps rate for investment grade and 50 to 70bps for high yield as companies reattach to fundamentals and markets start repricing fundamental credit risk.

Figure 16: US investment grade spread decomposition (in %)

Sources: Refinitiv, Euler Hermes, Allianz Research