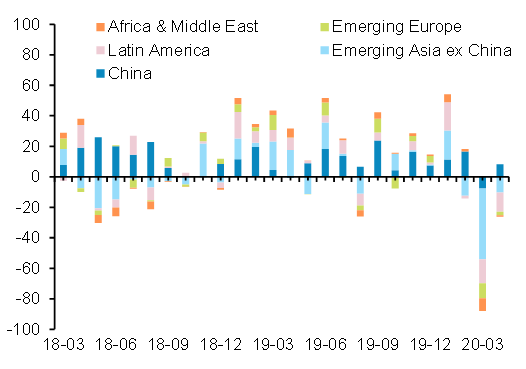

Capital outflows from Emerging Markets (EMs) bottomed out in March but could increase again should renewed trade tensions continue. Total portfolio outflows from EMs moderated to an estimated -USD18bn in April from the record outflow of -USD88bn in March. This reflects a turnaround in China (about +USD8bn inflows in April after outflows of the same magnitude in March) and a significant deceleration in other Asian countries, as well as lower outflows from Emerging Europe, the Middle East and Africa (see Figure 1). In contrast, portfolio outflows from Latin America remained substantial at -USD13bn in April (-USD16bn in March), largely due to much increased outflows from Mexico and Colombia, which were hit hard by the further slide in global oil prices last month. More generally, financial markets have begun to discriminate between rather resilient and more vulnerable EMs after withdrawing capital across the board in March when the potential size of the Covid-19 shock was still very unclear. The performance of EM currencies supports this view. After sharp depreciations in March, most currencies stabilized or even rebounded vs. the USD in April but a few continued to weaken, notably those of Brazil (-7%), Mexico (-4%), South Africa (-6%) and Turkey (-6%). Looking ahead, the renewed trade tensions between the U.S. and China, which have contributed to a softer start to the week in equity markets, could again lead to increased capital outflows, as occurred in August 2019 (-USD19bn) for example. Overall, however, we do not expect a month with similar outflows as seen in March over the next year.

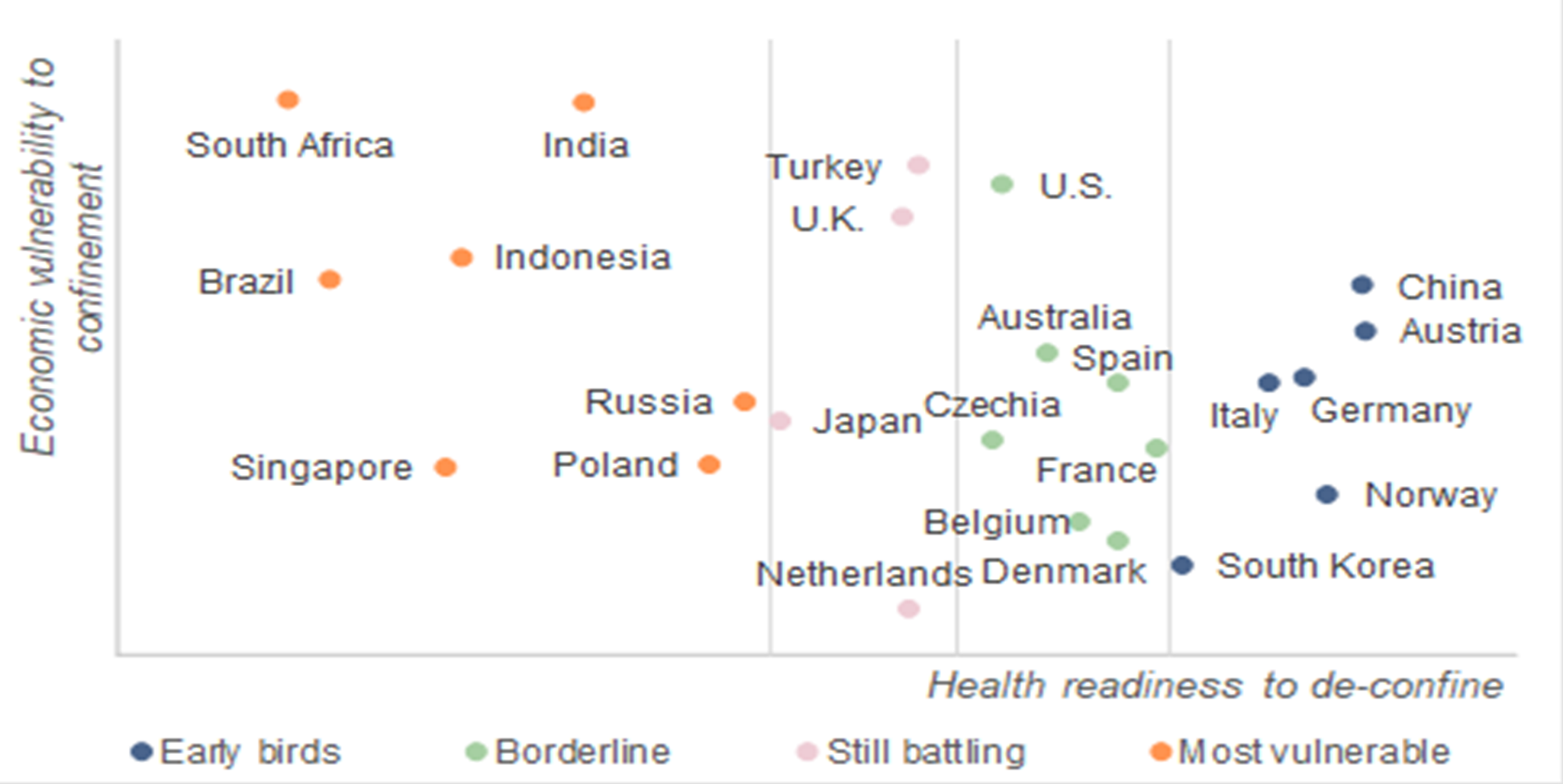

Weaker Emerging Markets may prioritize keeping the economy going, risking a high Covid-19 death toll. The economic cost of a full-blown lockdown is very high in many EMs. First, there are those with substantial structural weaknesses, such as a high dependence on exports of goods and services – and in this event in particular on exports of commodities and tourism services – a high share of informal employment and/or weak employment protection. Second, there are EMs that went into the health crisis with significant macroeconomic imbalances, such as large fiscal and/or current account deficits, a high dependence on external financing, low foreign exchange reserves and/or overvalued currencies. EMs that fall into these categories may opt to de-confine too early or to forgo confinement altogether in order to mitigate the slowdown of their economies. The aim or need to limit fiscal stimulus may also play a role. Figure 2 indicates that South Africa, India, Brazil, Indonesia and Turkey are large EMs with a high economic vulnerability to confinement. Hence, it is no surprise that both Brazil and Turkey, for example, have not imposed strict shutdowns (yet), even though their health indicators are also weak.[1] However, such a strategy carries the risk of a much more severe and lengthy sanitary crisis later on, which would eventually also hit the economy hard. For example, Turkish authorities emphasize that they want to rescue the tourism season of 2020 but this will be very unlikely if the death toll due to Covid-19 continues to rise.

Overall, the above analysis is consistent with our earlier conclusion that the following large EMs – Argentina, Turkey, South Africa, Mexico, Chile, Pakistan, Indonesia, Malaysia and Romania – as well as a number of Frontier Markets are most at risk of rating downgrades and subsequent sovereign and corporate defaults.[2]

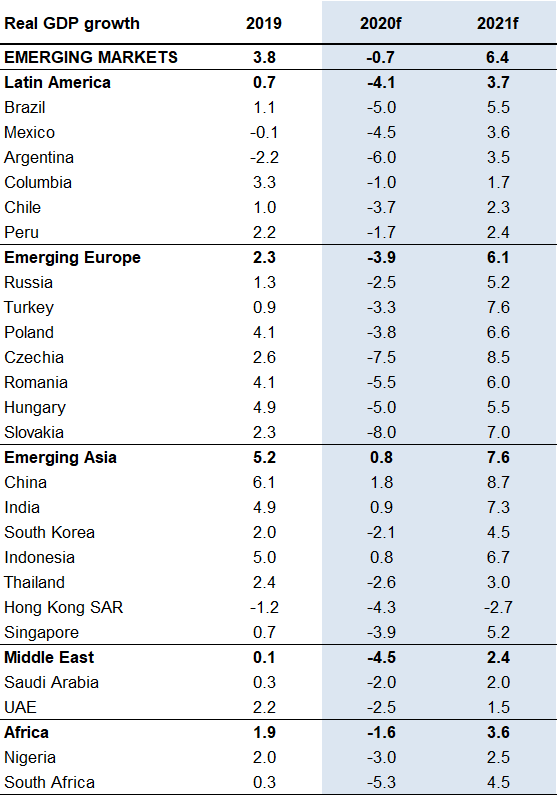

We continue to forecast real GDP in Emerging Markets as a whole to contract by -0.7% in 2020. Although capital outflows from EMs bottomed out in March, the real economies will continue to slide for now. Manufacturing PMIs of EMs released this week confirm a sharp deceleration of economic activity in April and a bleak outlook for the coming months. Our proprietary Composite EM Manufacturing PMI worsened to 42.3 points in April (from 49.6 in March). Excluding China, which is already in recovery (PMI at 50.8 in April), the composite index dropped to 34.0 (from 47.2). This supports our baseline projection of a steep economic contraction in the EMs as a whole in the second quarter, followed by a gradual recovery starting in the second half of 2020. We forecast EM real GDP to contract by -0.7% in 2020, followed by a strong recovery to +6.4% in 2021 (for details on forecasts for the main regions and key EMs see Figure 3).

Figure 1 – Total portfolio flows by region, USDbn