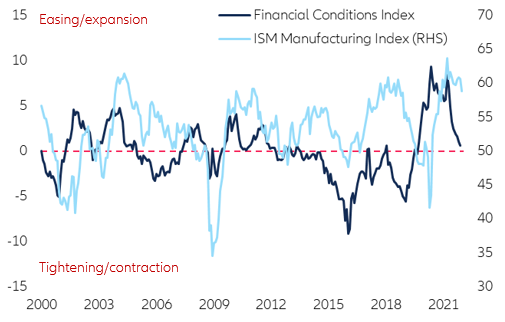

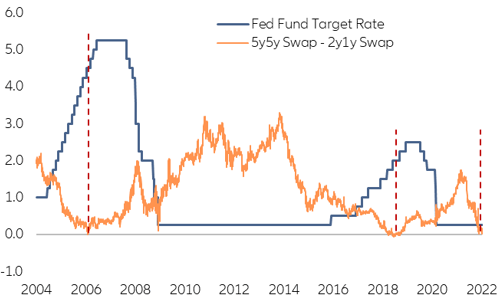

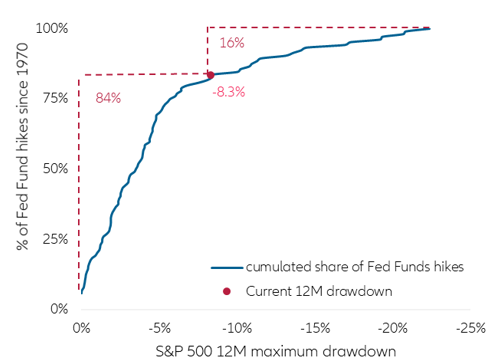

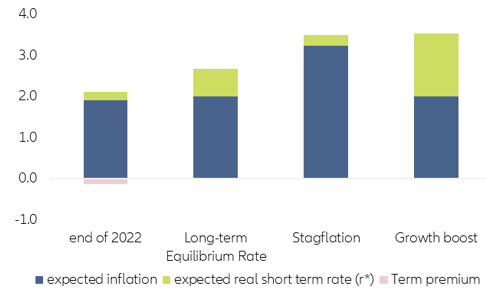

Executive summary

- While the rate lift-off might already start in March, signals are piling up that the Fed might break its hiking cycle after 2-3 hikes, much earlier than markets currently expect.

- The steepness of the US curve is very flat compared to earlier lift-off phases, swap Forwards shows inversion patterns that usually appear in late phases of hiking cycles and the 12-months drawdown of US equities is already at -8.3%. In the last 50 years only 16% of all Fed rate hikes occurred when the equity drawdown was that high.

- The main market risk might not be the Fed falling behind the curve, but investors being positioned too far ahead of the curve.

- Until the end of the year we see limited upside for 10y US Treasuries with quantitative tightening being the main upwards driver.

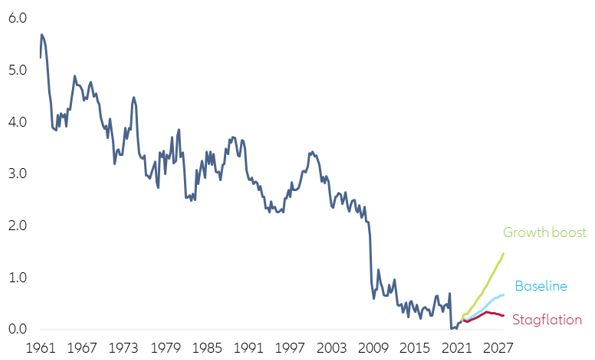

- Even in the longer run it is most likely that “low for longer” will prevail. Long-term rates clearly above 3% would require extreme monetary tightening, total deanchoring of inflation expectations or massive government spending with a permanent GDP boost.

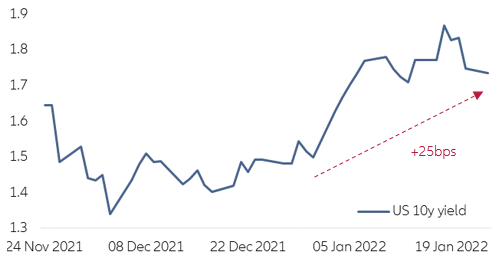

In early January, the US Federal Reserve’s communications pointing to more hikes and an earlier balance sheet run-off, together with CPI reaching a yearly rate of 7% in December, have triggered a surge in long-term US yields. Over a short span of two weeks, US 10y Treasuries yields rose 24bp from 1.5% to 1.75% and temporarily reached 1.9% (Figure 1).

Figure 1: Evolution of US 10y Treasury yield (last 2 months)