Source: Euler Hermes, Allianz Research

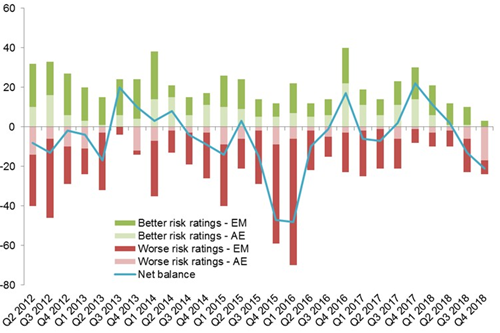

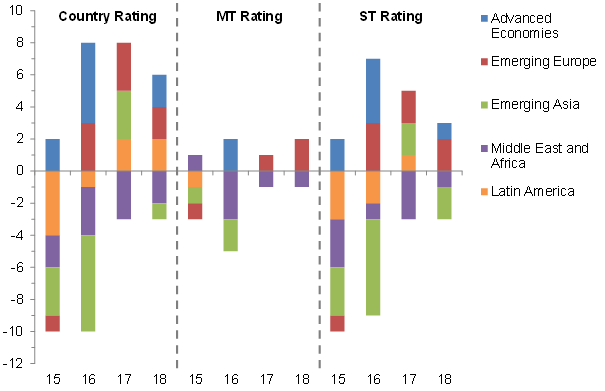

Our downgrades have rightfully identified the weakest economies in the loop. In the context of rising US interest rates and global liquidity tightening, policy mistakes in key emerging markets were particularly penalized in 2018. Policy mistakes will continue to play a key role, especially when they come along with existing or rising macroeconomic imbalances or with structural vulnerabilities. Among key emerging markets we have identified Brazil (weak public finances, policy uncertainty), South Africa (low growth and rising debt) and Russia (sanctions on financing flows, oil price) as tightrope walkers that could see a downgrade in 2019 in the event of renewed policy mistakes. More resilient but also on our watch list are India, Indonesia and the Philippines (rising current account deficits), Mexico (policy uncertainty) as well as Hungary and Romania (lack of policy response to counter overheating concerns). However, the majority of key emerging markets – especially those in Europe and Asia with current account surpluses – is well-positioned and should remain stable as long as the global trade environment stays relatively benign. That said, the net change in the Euler Hermes overall Country Ratings could move from net upgrades in 2018 (+3) to balance or a small number of net downgrades in 2019. As country risk ratings are forward-looking, this would reflect the continuation of the soft landing in 2020.

Regional outlook in 2019

The US to steadily decelerate as fiscal policy switches from a tailwind to a headwind

The US economy will progressively decelerate in 2019 as the impact of the 2017 stimulus fades away, whilst uncertainties regarding public debt sustainability are increasingly likely to hamper the investment cycle. Q4 19 will represent for us a turning point, during which another gridlock due to a government shutdown is likely to occur, damaging once more the general level of confidence. The growing perception by the market that public debt is not on a sustainable path will generate volatility and entrench the belief that austerity policy will emerge in 2020.

This anticipation of a budgetary U-turn in 2020 is likely to negatively impact growth via a much lower contribution to growth of both residential and non-residential investment. The investment cycle is also likely to be impacted by a deterioration of fundamentals in the US credit market as we have evidence that an excess of debt in the US economy has triggered a kind of anesthesia of price mechanisms. Credit spreads should rise in 2019 representing another blow to the investment cycle. All in all, we expect the US economy to grow by +2.5% in 2019 compared with +3% in 2018.

The Euro zone and the UK to be up to the challenge of political risk

The soft landing of the Eurozone economy after four years of above potential growth would be supported by (i) slightly more expansionary fiscal policy led by Germany; (ii) a moderate acceleration in private consumption; (iii) better external conditions, in particular concerning a positive impact from the fiscal and monetary stimulus in China in H2 2019 and resilient growth in emerging markets. Moreover, positive confidence effects from the resolution of major setbacks for confidence such as Brexit, the alleviation of the danger of additional tariffs on the EU auto sector by the US, the resolution of the US-China trade dispute, and in-check stress in Italy would also support growth. We estimate that this uncertainty “put” has cut as much as -0.3pp of GDP growth in Italy and the UK for example. However, the expected high polarization in the European political landscape post-EU elections where 39% of seats are likely to go to anti-establishment parties (with 16% for hard populists) could make EU voting procedures longer and create noise. In addition, the formation of the EU Commission for an appointment on Nov. 1st could take more time and pose additional difficulties.

Overall, the Eurozone slowdown is likely to continue with GDP growth at +1.6% at best in 2019 and +1.4% in 2020. However, risks are tilted on the downside given the negative base effects from the fall in production in Germany and sluggish consumer spending in France at end-2018. Inflation is expected to remain stable at around +1.7% in 2019-20 but should temporarily moderate in H1 given the recent fall in oil prices. Consequently, lower nominal growth should impact corporates’ turnover which had already lost -1pp of annual growth at mid-2018 compared to the year before. In addition, positive impact from lower oil prices could get compensated by higher wage growth and gradually less accommodative financial and monetary conditions which will have an impact on margins. However, given the challenging macroeconomic conditions the unwinding of monetary stimulus will proceed at a gradual pace at best in 2019. Assuming that the economic upswing in the Eurozone remains intact in 2019 we expect the ECB to raise rates for the first time since 2011 starting off with a +15bp hike in the deposit rate in September followed by a +25bp hike in all key rates in December. However, should economic growth disappoint we would not exclude a slower pace of the rate normalization. To counter any liquidity shocks the ECB will likely announce a new round of TLTRO funding in Q1 19 to support lending conditions.

Germany. Looking at country details, the overall economic situation in Germany can still be described as good despite the recent setback. The domestic economic conditions for a continuation of the upswing, albeit at a more moderate pace, are still in place. This applies in particular to private consumption. The disposable incomes of private households will continue to grow quite strongly in nominal terms in 2019. Real GDP growth is expected at +1.7% (from +1.5%), much lower compared to 2016-17 levels of +2.2%. That being said, the deterioration on the production side on the back of less supportive external conditions pose downside risks to our forecast that could be revised by as much as –0.2pp should end-2018 data confirm this negative trend.

France. In France, growth will likely be impacted by low consumer confidence and social tensions. These factors should trigger higher savings (15% of disposable income in Q4 18) and higher unemployment (9.2% in 2019, from 9.1% in 2018), with a possible -0.5pp impact on growth in a downside risk environment. Lowering inflation (+1% in 2019 down from +1.8% in 2018) will serve as a buffer, as it will support purchasing power and corporate margins, making the landing softer.

Italy. In Italy, despite the government embarking on a limited fiscal policy U-turn in December by promising to moderate its 2019 fiscal spending plan at least to some degree, economic momentum is unlikely to pick up markedly in the coming months. In fact GDP growth is expected to slow down from around 1.0% in 2018 to 0.6% this year. In our opinion, Italy will hardly reach the agreed deficit target of 2.04% of GDP given the weakening growth outlook, elevated borrowing costs, a higher structural primary budget deficit – due to the rollback of the pension reform – and no effort aimed at raising the economy’s growth potential. In addition, the expected strong results of Eurosceptic parties in the upcoming EU parliamentary elections are likely to strengthen the Italian government's confrontational stance against the EU over the course of 2019.

Spain. We see Spain outperforming its Eurozone peers again in 2019, while its gradual cyclical slowdown continues (+2.1%). Spain’s resilience can be partly explained by historically high profit shares (>43% of GVA) and subdued labor cost growth which allowed companies to invest. Reforms such as giving priority to company-level wage agreements (2012) controlled the wage increases despite employment gains. However, the domestic slowdown will accelerate in 2019 and 2020 (below 2% growth) as the 2018 budget has been rolled over in 2019 given the lack of parliamentary majority, meaning the fiscal adjustment will be stricter than advocated by the current government (-0.5% of GDP additional correction in the fiscal deficit). The probability of snap elections remains high since the governing socialist party struggles to pass legislation while leading opinion polls.

UK and Brexit. Our Brexit central scenario continues to be a last minute blind deal between the UK and Europe (including an extension of Article 50 beyond March 29). This will give scope for the sterling to rebound to 1.15-1.20 against the EUR on average in 2019. However, as high uncertainty remains, we continue to give a 25% probability to a no Brexit deal. While general elections are less likely after Theresa May won the confidence vote from her party, we as also include as an end scenario a second referendum on the Brexit deal which will ultimately require the extension of Article 50. Economically, the longer uncertainty remains, the weaker the UK economy will become which is already visible in the depreciation of the pound sterling and general living standards of British households (with a current savings rate at 4.4%). The prolonged uncertainty doesn’t come without costs: we calculated that it costs at least -0.1pp of growth to the UK every quarter and GDP growth should reach +1.2% in 2019 and +1.0% in 2020.

China to intelligently fine-tune demand policy

Looking ahead, 2019 will not be a walk in the park. Firstly, since the beginning of the year the news flows from corporates that are usually seen as bellwethers of the Chinese economy have not been encouraging with several profit warnings (Apple, Samsung). Secondly, bad news from the car industry (first drop in 20 years) suggests that private consumption could be not as strong as expected. We argue that there is still room to grow although the pace of expansion will likely be slower (+6.3% in 2019 after +6.6% in 2018) due to: weaker growth in exports as global demand softens; slower growth in domestic demand as policy stimulus remains prudent and industrial corporates struggle due to lower sales growth. Household’s consumption will likely be the main driver. Fundamentals are relatively solid. Unemployment rate is low (surveyed unemployment rate in urban areas at 4.8% in November) and income is growing at a solid pace (+8.7% estimated in 2018 for per capita disposable income). Credit to households is growing at a fast pace (above +15%) and fiscal policy is becoming increasingly supportive (authorities raised personal income tax threshold, and several tax deductions on expenditures such as rent and healthcare have been implemented this year). Inflation pressures will likely remain limited (+2.5% in 2019) helped by a continued opening (lower tariffs) of the economy and low oil prices. On the corporate side, demand will likely be moderate hindered by lower sales (for exporters, commodity producers, e.g.) and a still elevated level of debt (155% GDP). Public sector expenditures are expected to get traction in the form of higher infrastructure expenditures and more spending from State Owned Enterprises.

Emerging economies should exhibit resilience amid divergence

Growth is expected to stabilize in Emerging Markets. This outcome could result from two conflicting forces. First, monetary policy tightening in the US was the main issue of 2018 and is expected to go progressively on hold in 2019. Inflation will likely be lower in 2019 in the G3 ( US, Eurozone and China) as a result of lower oil prices. Thus, the pressure on EM currencies as a whole will likely lower. However, as growth will decelerate in the G3, each EM area will be exposed to lower demand from its main partners. Moreover, lower growth should also mean lower demand for commodity exporters. China is the case in point, as current low levels of manufacturing activity leads to lower import growth expectations, negatively impacting Latin American and African economies. Eastern Europe is also exposed to lower growth in the Eurozone, particularly in Germany.

Summarizing these external factors, EM should exhibit resilience amid divergence. Policy buffers are now wider in many areas compared to some years ago. Current accounts show surpluses in many Asian and Eastern European economies and were rebalanced in many others (e.g. in Brazil). The divergence will be driven by the trade exposure as well as the degree of domestic policy heterodoxy, particularly triggered by renewed tensions on commodity exporters. E.g. in Brazil, higher risk spreads should impact corporate borrowing costs, despite a modest growth acceleration (+2.3% up from +1.3% in 2018). Divergence may also expose some EM markets to bouts of exchange rate weakness. Lower demand in the G3 should add to that by triggering exchange rate undervaluation policies, particularly in Emerging Asia. Africa will likely face the higher downside risk, since many countries will organize elections in 2019, amid a rise of armed conflicts in Central Africa and increasing social protests particularly in North Africa. Against this background, we also see a potential for orderly tensions resolution, since many countries made progresses in terms of overall governance (e.g. Morocco, Kenya, Rwanda).

Alternative scenarios

A coalescence of risks to possibly trigger a forced landing

Our central scenario hinges on the assumption of favorable denouements in different perilous situations. There is for example a non-negligible possibility for trade negotiations between the US and China to turn out badly. In such circumstances, global trade could rapidly head toward a regime of lower growth in which the probability of a recession could significantly increase in particular for export driven economies. This probability would be nurtured by a severe correction of the equity market in conjunction with a severe deterioration of credit quality. In the meantime, the quality of coordination in economic policies, after two years of America first policy, would have significantly deteriorated. In the absence of concerted answer to a rapid deterioration of global macroeconomic conditions, the world economy would experience a brisk deceleration bringing growth durably below its potential. We attach a 25% probability to this scenario.

Tail risk scenarios

We have identified 5 different tail risks: a generalized trade war, the burst of the US credit bubble with a systemic dimension, a default of the Italian debt, a freezing of China’s capital market and a stranded asset shock.

- A generalized trade war. US average tariffs rise to 12%. Global trade is 6pp lower, and global growth 2pp lower compared to our central scenario.

- Burst of the US bubble with systemic impact. The burst of the US credit bubble requires a state intervention with further and unsustainable deepening of the US deficit. A run on the USD and Treasuries has a devastating impact at a global level.

- A default of the Italian debt. Italy’s government sticks to a highly expansionary stance of fiscal policy. Credit downgrade follows to non-IG in 2019, banks lose access to ECB liquidity but the Italian government refuses to accept an ESM program. Spreads climb above +700bp, Italy falls into a deep recession. Due to significant contagion, particularly to the periphery, the Eurozone economy also contracts. ECB implements significant non-standard measures

- A freeze of China’s capital market. Defaults of large state-owned financial institutions trigger a freezing of monetary and capital markets. Large capital outflow occurs while the PBOC is unable to stabilize a steep fall in the CNY. Global equity also experiences a huge selloff.

- A stranded asset shock. Financial markets suddenly realize the loss of value related to stranded fossil fuel assets. The effects of a carbon bubble burst results in wealth losses estimated between USD 1 – 4 trillion, a correction similar in size to the sub-prime crisis.