Executive summary

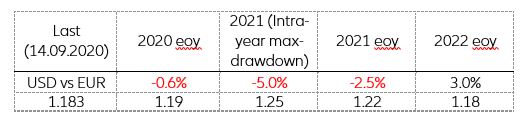

After its peak on 20 March 2020, the USD has depreciated 10% against the EUR (1.174 as of 21 September 2020), going back to levels last seen in mid-2018. This rapid depreciation has raised many questions about the future of the dollar. Though forecasting exchange rates is a form of Holy Grail for forecasters, we decided stick our neck out and present our methodology that separates short- and long-term factors affecting the price determination of the EUR/USD exchange rate, and our results:

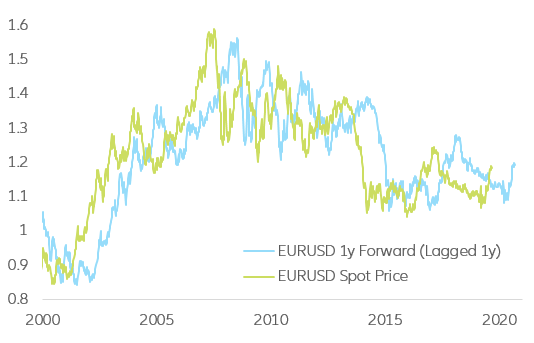

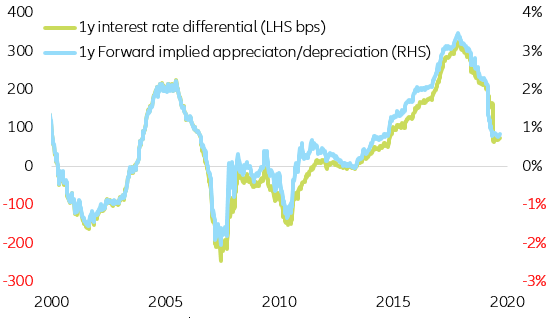

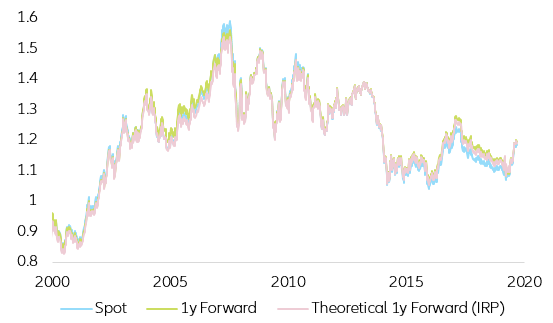

- Due to the recent anchoring of both USD and EUR short-end of the curves, by their respective central banks, Forward EUR/USD rates contain no relevant information about the future path of the EUR/USD exchange rate.

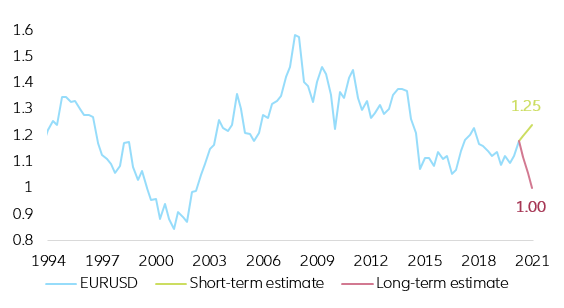

- Our modeling approach based on the U.S. balance of payments hints at a mild appreciation of the USD vs. the EUR in the mid- to long-term (converging towards parity in the long-run). Nevertheless, this methodology does not reveal much information about short-term developments.

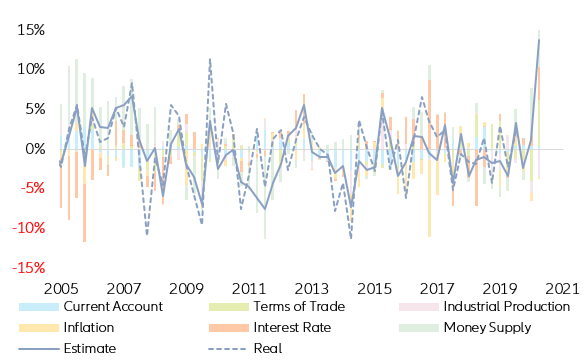

- Our monetary model suggests that if current economic and financial dynamics do not suddenly change, the dollar is set to depreciate versus the EUR by up to 5% (~1.25) within the next 12 months. Yet, it also suggests that if the U.S. would start reverting to pre-Covid-19 dynamics, the EUR/USD would start a slow but steady climb towards parity.

- Overall, by combining both balance of payments and monetary approaches, and under the assumptions that the Covid-19 economic shock is set to fade away in 2021-2022 and that U.S. funding dynamics are set to slowly converge to pre-Covid-19 trends, we conclude that the USD can depreciate by as much as 5% (~1.25) in the next 12 months. Thereafter, it could resume its upward trajectory, slowly converging at a 2 to 3% annual rate towards parity.