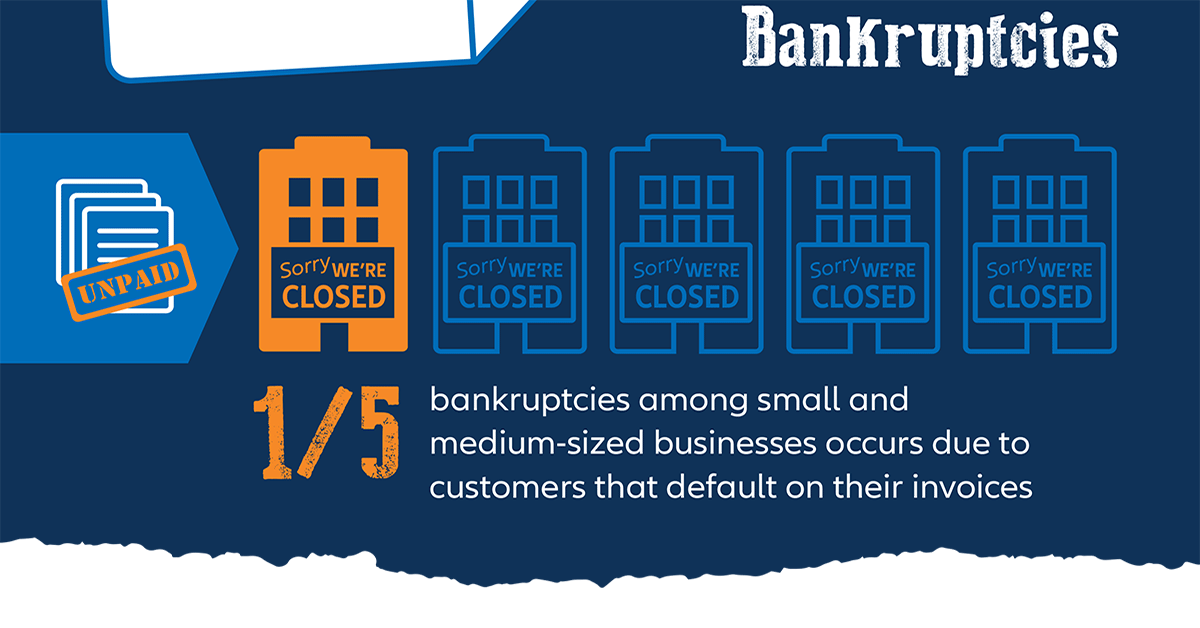

Finding the sweet spot between these two extremes is essential to your company’s future. Of course, it isn’t possible to eliminate all credit risk. However, a strong approach to credit management can streamline credit approvals at all stages of the customer relationship.

Credit insurance plays a key part in this process. Not only does credit insurance provide unmatched information about customers’ financial health, it also provides a payment guarantee in case of an unexpected loss.

Companies can also take steps on their own to improve their credit management and ensure that they always have a good grasp of their risks. Here are nine ways to do so:

- Know your customers. By researching customers before signing contracts, your company will understand the strengths and weaknesses of each one. Using this insight, you can make more strategic credit decisions throughout the customer relationship.

- Clearly document terms and conditions. Disputes and misunderstandings about invoices can create major delays in receiving payment. By clearly articulating the terms and conditions of the credit relationship to every customer, you can avoid many of these situations.

- Get receipts. Another area of potential conflict is whether and when a customer receives the purchased products and services. Creating and requiring customer signatures on receipts for all transactions can help minimize any questions.

- Bill quickly. Sending invoices as soon as a transaction is complete starts the customer’s payment process as quickly as possible, increasing the chances of timely payment.

- Call on or before the due date. A friendly reminder that an invoice is due or coming due is an important way to let customers know that you are tracking payment and expect a timely remittance.

- Schedule periodic payment reminders. One reminder that an invoice is due may not be enough to get customers to pay. If the “squeaky wheel gets the grease,” the vendor who issues reminders regularly and in a professional way is more likely to receive payment within the expected timeframe.

- Document and communicate the payment process. Everyone in the organization must understand, comply with and support the company payment policies and process. Mixed messages and poor communication to customers will only create confusion and delay the payment of invoices.

- Regularly review customer financial information. It is often tempting to overlook any negative change in a customer’s credit or financial status, especially when the customer is a large, profitable and long-term one. However, circumstances change and a customer that once represented a low risk and regularly paid invoices on time may slowly or suddenly delay or miss payments entirely. Companies must review and consider any new financial developments without bias when managing credit decisions for a specific customer

- Be consistent. To be successful, you must apply all of the steps in your credit management process to all customers and for every transaction and invoice. Only by being consistent can you ensure that customers make every payment in the timeliest way possible.