- Innovation in electric vehicles (EV), autonomous driving and new mobility services, boosting R&D spending, capex, M&A and partnerships

- Public subsidies for EV and regulatory requirements in top markets, notably China

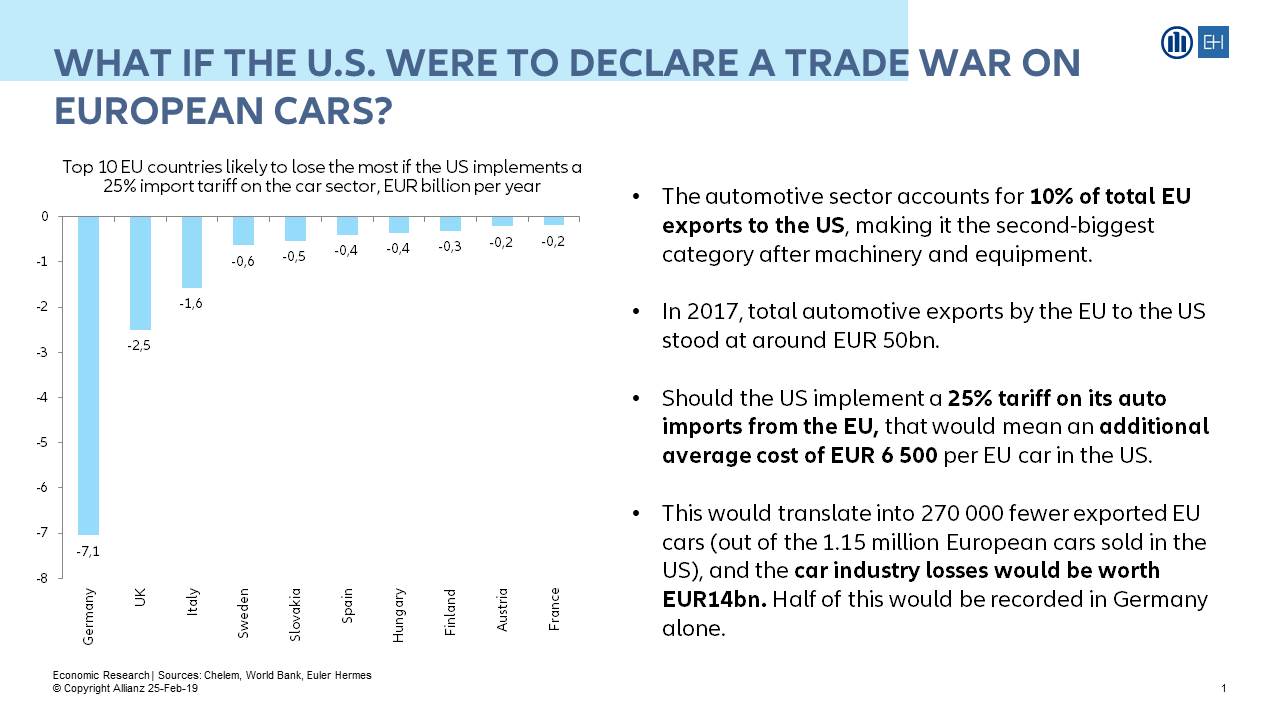

- Downturn in US car sales and rapid decline of diesel in Europe

- Supply chain strategies in response to the outcome of NAFTA renegotiation and to Brexit uncertainties

Solid perspectives in sales, with faster and challenging market’s transition to EV

The Automotive market is on course to cross the 100 million units’ threshold in 2019. In 2018, global sales in new vehicles should exceed 98 million, posting a +2.5% increase. Positive forecasts in private consumption and corporate investment, fueled by rising incomes and still low interest rates, will support new registrations in passengers’ cars (74% of the total) and commercial vehicles (26%) in the majority of countries.

Yet, the automotive industries face challenging times. One issue is their ability to cope with the uneven tempo of markets. We expect a continued growth in China (+3% to almost 30mn units) and most of the European Union (+2%), a recovery in Russia (+5%) and Brazil (+3.5%), a stabilization in Japan and South Korea, but also two major exceptions: the U.S (-2% to 17mn units) and the UK (-6%). The second challenge is to manage market’s transition, notably to EV and connected cars, while keeping on meeting each market demand and the diversity of regulatory frameworks. New models are crucial to stay competitive, from low costs to premium cars and all kinds of EV; the latter will keep on a double digit trajectory with 1.7mn registrations in 2018 and a fleet of 5mn cars (compare to a total of 1.4bn vehicles in use worldwide). At the same time, emission requirements are intensifying, increasing the costs of cars and the pressure on manufacturers, notably in China where the draconian new rule coming into force in 2019 is undoubtedly already a game changer for car makers.