The Crown Preference – what is it?

As many companies face credit risk for the first time in this period of economic instability, it is worth noting that HM Revenue & Customs (HMRC) now ranks ahead of Floating Charge Lenders and Unsecured Creditors on the ladder of creditors when a UK company faces insolvency.

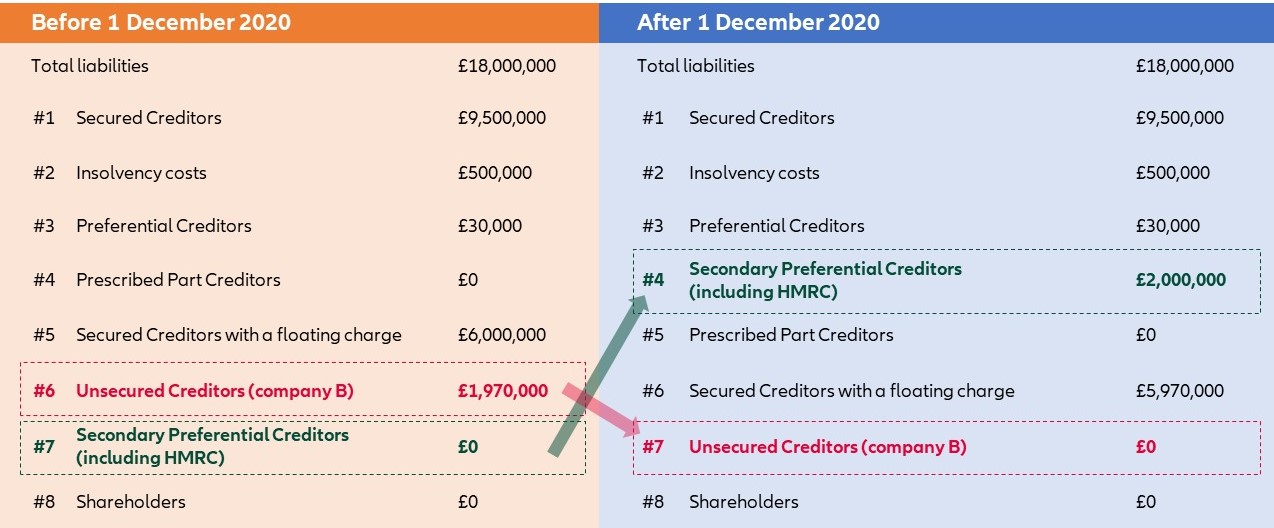

The order of preference in insolvencies since1 December 2020 is:

- Secured Creditors (often fixed charges i.e. mortgages).

- Insolvency costs.

- Ordinary Preferential Creditors (primarily limited to certain employee claims).

- Secondary Preferential Creditors (this will include certain HMRC taxes now - VAT, PAYE, Employee NI contributions, student loan contributions and contributions to the construction industry scheme).

- Prescribed Part.

- Floating Charge Holders (normally includes finance companies who may have some security on products such as invoice finance).

- Unsecured Creditors (including HMRC for non-Secondary Preference debts).

- Shareholders.