- As the parties to COP 24 gather in Katowice to agree on implementing the Paris agreement, there could be a step up towards the reality of assets having to leave the market and others coming to displace them. The UNFCCC Executive Secretary told participants that climate change could lead to productivity loss in the order of USD 2tn by 2030. We estimate that c USD 1.4tn in the energy sector alone have already been lost between 1997 and 2017, and that future loss of value from stranded assets could range from USD 0.3tn to 1.6tn. Coal assets alone could lose value in the order of USD 550bn to 2035. We expect wide spread impact across a number of sectors, first and foremost energy, thus our focus in this paper.

- Beyond coal power plants as the first obvious casualty, risk affects upstream assets, infrastructure, components and equipment, contracts and services. We see an inflection point in relative returns, with ROCE (return on capital employed) of our low carbon basket exceeding that of the high carbon basket for the first time in 2017, by 2.3pp. Asset stranding amongst others is at the origin of some the major energy company splits.

- Execution, regulation and counterparty risks call owners, investors and stakeholders for a selective and dynamic approach. First, new supply companies face greater risk related to volatile wholesale power prices. Second, regulated activities take a greater weight within group structures, and there may be material revisions to regulatory returns in networks and associated activities. Last, financial strength of exposed businesses has reduced, as a result of previous strandings. Further asset losses might put entire business lines into question. Balance sheet stability is at stake if large assets have to be written off and are no longer available as financing collateral.

The global economy stands the risk to lose large amounts of value from assets becoming unproductive and misallocation of capital. While the debate about the various forms of stranding of assets is alive, and the process has already begun, we believe there is considerable scope for further accelerated loss of value from sources yet not fully appreciated. We focus on energy as the first immediately affected sector.

Which types of assets are prone to become stranded assets?

Needless to elaborate, power stations are most immediately affected assets, specifically coal powered plants. Directly associated are the assets of the entire coal supply chain including the mining sector and its supply chain. We recognise the strength of Asian coal demand resulting from close to 300GW of new coal plant build to 2022, most of which in China. However, we argue that this very plant is at high risk of later stranding along with its connected industries, even if it supports a coal value chain over the medium term. We have included these assets in our global calculation below. We believe there is enough value in terms of contribution to system security and other services for gas, particularly CCGTs (combined cycle gas power turbines, the most efficient gas plant), that we do not count them in at this stage. That is a question of the time horizon. Large parts of the global gas fleet may only become stranded at a very late stage (see below). The oil sector is heavily exposed both as a direct emitter and energy intensive sector. Oil fields, particularly tar sands, have become riskier, as have refineries. Reduced utilisation rates may affect pipelines, vessels and midstream infrastructure. Industrial plant across all sectors that is either energy intensive or emission heavy in its own right or dependent on a CO2 heavy end customer is of concern. We point to steel manufacturing, automotive, pulp/paper, and fertilisers as a non-exhaustive list, even though we do not analyse them in this paper.

When will assets become stranded?

We see key catalysts for stranding in the context of climate change: A step up in CO2 prices, currently occurring and already partially stranding assets, the next leg up in emissions reductions and prices in Europe and elsewhere, business adjustment for a 2 degree scenario as per the UN Framework and IEA’s new policy scenario, and lastly adjustment of the target beyond a 2 degree scenario. We see three stages of coal phase out: A first phase of reduced load factors which has already begun, inefficient plant leaving the market and transition to CCGT; supported low carbon systems through the 2020s with early full phase outs in the mid-2020s; and lastly full end of coal from the mid-2030s to 2040. Gas will in our view retain residual value due to its critical functions. But, there is business as usual in gas and oil, according to our gage.

How much value could be lost?

As a first step, we consider historic stranding. In order to isolate climate change from other factors, we have looked at a depreciation based approach for the US. Our intuition is that a process of an over-elevated consumption of fixed capital under this definition can be associated with stranded assets. A trend analysis in long term time series of amortisation by relevant sectors since 1947 (source: US Bureau of Economic Analysis) reveals a break in the trend of the mining, –oil and gas sectors from 1997 onward suggesting a new regime of capital depreciation post signature of Kyoto protocol. Consequently, we have decided to calculate the difference between what has been observed in terms of depreciation and the theoretical path of depreciation for diverse sectors, maintaining a trend prior to 1997-2017 era.

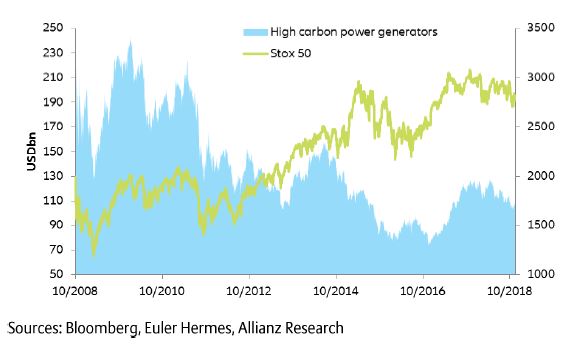

Our estimate of stranded assets, based on a normal trend of depreciation and what has been observed, shows that oil and gas has registered an approximate cumulated loss of more than USD 1 trillion between 1997 and 2017, while utilities and construction follow with USD 347 bn and 350 bn of losses respectively. European utilities have been particularly affected by climate change induced energy transition and loss of asset value. Our basket of European coal generators has lost USD 167bn of market capitalisation between 2008 and 2016 whereas the broader market has added Eur 800bn over the same period.

Figure 3: Market capitalisation European high carbon power generators vs Stoxx 50