- The mid-term elections and the resulting Democratically controlled House does not change our US economic outlook. GDP is still expected to grow by 2.9% in 2018, and 2.5% in 2019. However, businesses could be affected by policy shifts in six areas: infrastructure spending, regulation, taxes, public budget, trade and immigration.

- We do expect bipartisan policy support to businesses when it comes to additional infrastructure spending (USD200bn financed by increased taxes on gasoline), regulation (negative for the pharmaceutical sector, positive for the financial sector), and to a lesser extent, further tax cuts (reinstatement of State and Local Taxes deduction, and new Qualified Opportunity Zones).

- There will be strong opposition on voting on the budget with foreseeable last minute gridlock and shutdown risks. Federal deficit and debt will continue to increase, leading to a tightening of financial conditions and higher recessionary risks. As a result, the probability of a recession could increase from 15% to 25% by the end of 2019. Leveraged businesses such as utilities and materials could suffer.

- On trade and immigration, softening and compromises could come from the change in the political landscape. This could benefit the agriculture sector (tariffs, and workers’ visas), wholesale and retail sectors, as well as business with China more generally.

Outcome of the 2018 US mid-term elections

The Democratic Party won the House of Representatives Tuesday night while the Republicans still rule the Senate. The result was not unexpected because since 1946, an unpopular President’s party has lost an average of 37 seats. We will therefore have a divided Congress for the next two years, and as a result, legislative gains may be minimal. However, that’s not different to what we have had in the first two years of the Trump Administration, because with the exception of tax cuts and the appointments of two US Supreme Court Justices and scores of lower Court judges, the Congressional accomplishments during the first two years of the Trump Administration were small. Most of its accomplishments were done through rules and Executive Orders, including an immigration ban, imposing steel tariffs, rewriting the Affordable Care Act, changing and no longer defending Obama era environmental regulations and withdrawing from the Paris Climate Accords and Iran agreements. Now that the Democrats have taken control of the House, we can expect that the President will continue to use rules and Executive Orders to further his agenda.

We look into six policy areas and their respective impacts on businesses.

1. Taxes

The House has already voted for making 2018 tax cuts permanent (they have to phase out in 2025) for small businesses and individuals. But now that the Democrats have won control of the House, they have no reason to cooperate, even as the budget deficit gets worse and causes concern in the stock market. Tax extensions bring anger from the blue state Democrats who feel that the disallowance of most of the deductions for state and local taxes (SALT) was specifically directed at their states such as California, Minnesota, Massachusetts, Connecticut, New Jersey, Illinois and New York.

However, there may be some much needed technical corrections to the hastily drafted Tax Cuts and Jobs Act provided that the Democrats are able to get something out of it. Some of the logical areas might be: 1) enhancing incentives for retirement savings for low income individuals; maybe 2) raising the maximum SALT deduction somewhat above its current $10,000 limit (for middle and upper middle class people but not the rich), and; most probably 3) extending the “Qualified Opportunity Zones” program, which consists of reinvesting capital into economically struggling areas.

Impact for businesses 1: “Qualified Opportunity Zones” provide a new potential source of financing incentives for businesses looking to relocate or expand. Extending the zones will have an important impact in terms of relocation of activity. Raising the SALT deduction should help the real estate industry in states which were clearly impacted by the elimination of the SALT deduction. In the short term, in 2019, we consider this positive impact to reduce by -5% the probability of recession in the US. However, small businesses should probably be less hopeful approaching 2025 as there is a low probability for the extension of tax cuts thereafter.

2. Infrastructure plan to have more traction

This could be the potential meeting point for next year. The logical compromise is to raise gas taxes, promote more public private partnerships and increase state funding. President Trump’s initial program planned USD200bn of government seed money being augmented by private funds totaling USD1.5trillion of investment in infrastructures over ten years. Only USD21bn out of the USD200bn announced by the government have been spent for now. Infrastructure spending helps generate jobs for private sector unions close to the Democratic Party, and it could add a little juice to the economy, which is expected to decelerate in 2019 at 2.5% yoy compared with 2.9% yoy in 2018. In terms of funding, the Federal Gasoline tax rate has been unchanged since 1993 and is at 18.40% today. We estimate that a rise to 22% would provide USD40bn/year of revenue and in five years it would cover the USD200bn needed for the infrastructure plan. The multiplier impact on GDP should be weak as this program will be funded by tax hikes penalizing low revenues and the middle class. The impact on growth would be neutral as fiscal multipliers of infrastructure projects and (negative) transfers of individual are pretty close (respectively 1.3 and -1.25).

Impacts for businesses 2: The following sectors are expected to benefit from infrastructure spending: cement suppliers and other building material companies, companies providing roofs, floors and plumber, companies supplying machineries of construction, companies offering infrastructure engineering services as well as private equity funds providing private capital.

3. Debt intensive sectors to suffer from financial instability resulting from budgetary blockages

The result of this new political configuration is a probable polarization of positions on budgetary issues, and numerous blockages in discussions, meaning a continuously rapid deterioration of fiscal deficit (we expect a deficit at 3.7 % of GDP in 2018 and 4.5% of GDP in 2019). The usual last minute theatrics are expected, but eventual passage of budget will be the outcome, however the budget drama will create substantial bouts of volatility contributing to a significant tightening of monetary and financial conditions, beside the ongoing normalization of the monetary policy operated by the Fed. We consider this uncertainty to add 10% to the current level of recession probability.

Impact for businesses 3: We identify the sectors being the least favorably positioned in terms of sustainability and instability of the debt. Our debt sustainability ranking (based on an analysis of four different variables of credit risk, i.e. EBITDA/interest expense, total liabilities/common equity, short term debt / total liabilities, interest expenses / total debt of S&P500 companies) identifies Basic Materials and Utilities as being the most exposed to any significant tightening of monetary and financial conditions. These sectors should therefore be closely monitored.

4. Trade policy may be less extreme

On trade issues, Trump, who has dramatically deviated from the free trade positions of all the last six Republican Presidents since World War II, might be able to secure some Democratic support, since they, and not the Republicans, have traditionally been more resistant to free trade. However, Democrats will demand enhanced environmental, safety, and worker income standards. The recent NAFTA/USMACA will probably be validated since there has been a collective sigh of relief from the business community that the Administration did not destroy supply chains, left most measures intact, and perhaps even improved a few things.

Can Congress intervene in the Section 232 metals tariffs, or the tariffs imposed on China, or the threats against German cars? The rhetoric and the actions of the Trump Administration have been blunt and forceful but thus far do not seem to have accomplished much, as the Chinese are playing a long game and have begun by retaliating or finding new sources for agricultural products, significantly harming the American heartland. China is playing hardball and it has some strategic advantages that other nations might not, such as a strong influence over North Korea.

As evidenced by the NAFTA/USMCA agreement, the President is more flexible on trade than he appears, and this is enhanced by his unique capability of claiming victory regardless of whether or not it is real. In the NAFTA/USMCA negotiations, pressure from the business community helped bring him to the table to sign a deal which would protect the US economy and well-paying union jobs. A Democratic House will help curb President Trump’s more extreme trade policies.

Impact for businesses 4: President Trump will be inclined to find an agreement after a few concessions from China. If he can negotiate the removal of tariffs on US agriculture products, as well as the requirement for US companies to form joint ventures and share technology if they want to operate in China, then he could claim victory. Winners will be the agriculture and technology sectors, and wholesalers and retailers. However some lasting damage may have been done as the Chinese look for new food supply sources, and US manufacturers, either exporting products to China or who have facilities there, might face new burdens making this market less appealing. This attenuation of trade risk could reduce by 5% the probability of a recession.

5. Regulation: Healthcare, retirement, Chevron Doctrine and financial de-regulation

Drug prices: More transparency in drug pricing is needed and Trump has targeted the issue, saying “Americans pay more so other countries can pay less”. Indeed, a report released on October 25 said that Medicare was paying 80 percent more for drugs than other countries.

Savings plans: There is a general consensus that changes to the 401k system could occur, most notably allowing small unrelated employers to pool together to create plans. The intent of the plan is to expand the universe of companies offering retirement benefits.

Review of Chevron Doctrine: The Supreme Court is likely to review a case challenging the Chevron Doctrine. That 1984 decision basically gave great deference to Government agencies writing regulations, and said that those regulations could only be invalidated if they were arbitrary and capricious. Business groups have been fighting this for a long time, arguing that the deference was too broad. Conservative Justices on the Supreme Court have signaled that the 1984 Chevron decision has gone too far and demands a new look.

Financial de-regulation: continuing financial de-regulation in favor of households (the revision of FICO scores is expected to significantly improve credit scores of millions of Americans) and in favor of regional and small banks will help boost credit for households and small businesses. However, the accumulation of risk in the banking system, following a wave of financial de-regulation already put in place, could in our view add 5% probability to the risk of recession in the US.

Impact for businesses 5: pharmaceutical companies could suffer an erosion of their profitability; financial services firms could benefit if businesses want to form 401k pools; de-regulation will continue to boost the supply side of the economy as a whole, and; small companies are likely to benefit from easier access to credit. However, we should mind the accumulation of risk in the banking and financial sector again. As former Fed Chair Yellen said “There are a lot of weaknesses in the system, and instead of looking to remedy those weaknesses I feel things have turned in a very deregulatory direction.”

6. Immigration and labor costs

Concessions on immigration issues might be the price the Trump Administration has to pay in order to get a budget and a debt ceiling agreement. A resulting immigration reform package could include: 1) funding for the Mexican Wall; 2) legal Status for DACA immigrants who came to the country with their undocumented parents when they were children; 3) greater number of visas allowed for agricultural workers needed for farm production, and; 4) enhanced immigration enforcement.

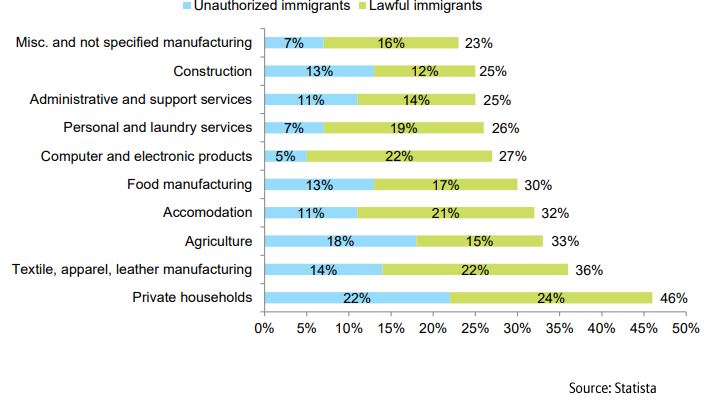

Impact for businesses 6: Agriculture should be a winner but other immigration intensive sectors (textile, accommodation and private households, Figure 1) could observe a significant rise of their labor costs as immigration becomes more difficult. Salaries have accelerated at 3.1% yoy in October 2018. A tighter control of immigration beside the agricultural sector could add pressure on average salaries and therefore increase the risk of a more rapid than expected rise of US interest rates, therefore adding 5% of probability to the risk scenario of a recession in 2019.

Figure 1: Industries with the most immigrant workers